The cost business insurance for gyms and fitness centers averages around $90 per month, or roughly $1,085 per year, across the six most common coverage types. MoneyGeek's analysis covers gym and fitness center businesses with one to four employees across 50 states and Washington, D.C., at standard policy limits of $1 million per occurrence and $2 million aggregate, except workers' comp, which follows state-mandated limits.

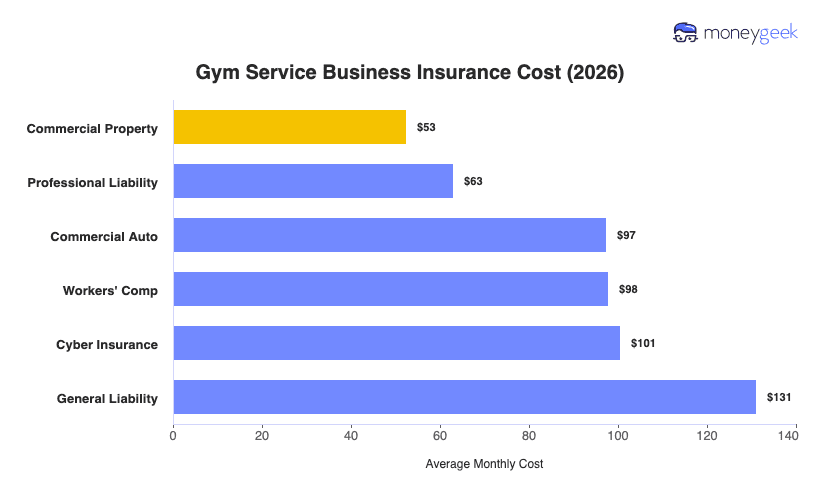

By individual policy, costs range from $53 per month for commercial property to $131 per month for general liability, a gap that reflects how differently insurers price these risks for gyms. Commercial property prices at the lower end because your facility and equipment represent a fixed, known asset with predictable replacement value. General liability lands at the top because members can sustain injuries during class, on equipment and in common areas.

The table below shows average monthly costs for each coverage type, but treat these figures as benchmarks, not quotes, since your actual premium will vary based on your specific business profile.