The average cost of business insurance for tax preparers is $50 per month, or $598 per year, averaged across six common coverage types, using standardized profiles for businesses with one to four employees and $1 million per occurrence limits.

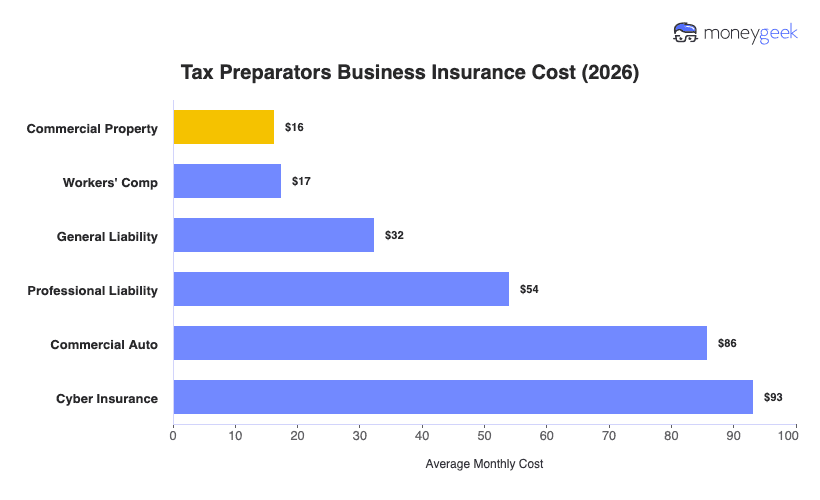

For a single coverage type, your cost will fall somewhere from $16 to $93 per month. Commercial property sits at the low end as tax prep offices typically carry modest equipment and operate from small offices, so insured values stay low. Cyber insurance prices highest because tax preparers collect Social Security numbers, bank account details and financial records for every client.

The breakdowns below are benchmarks as your actual premium depends on your business profile: