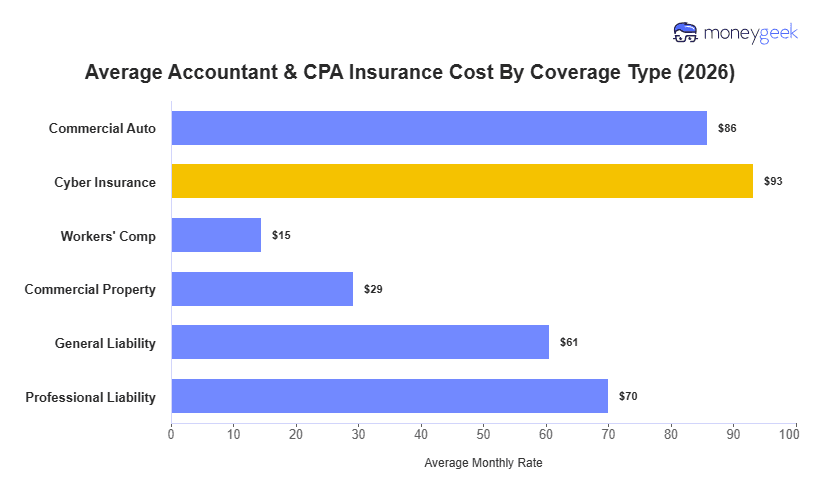

Accountant and CPA business insurance averages $59 per month, or $707 per year, across the six most common coverage types. Our analysis modeled businesses with one to four employees across all 50 states and Washington, D.C., using policy limits of $1 million per occurrence and $2 million aggregate.

Individual coverage costs range from $15 to $93 per month, with workers' compensation pricing lowest because desk-based accounting carries a low injury-risk class. Cyber insurance anchors the high end, driven by the tax returns, payroll records and financials accounting firms hold. You likely expect professional liability to be your largest cost since it's the coverage the profession is built around. Our data, however, says otherwise: cyber insurance prices above professional liability for a practice like yours. That reflects how much data density shapes financial services business insurance costs alongside professional risk.