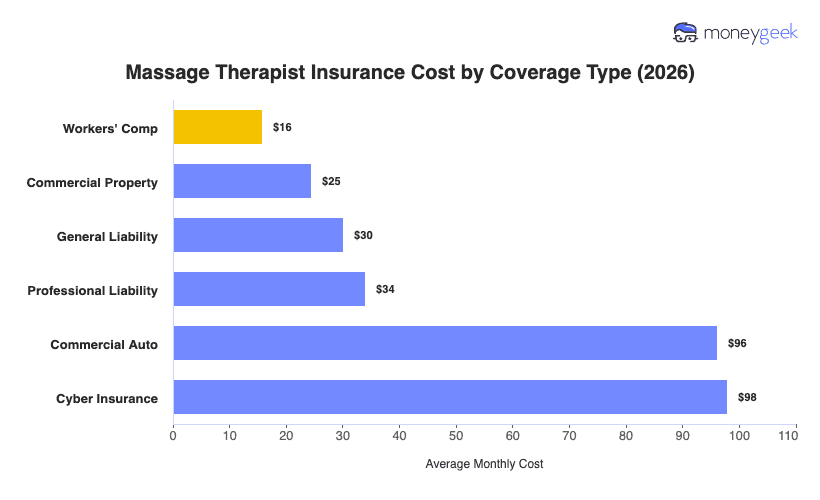

Business insurance costs vary widely across the beauty and wellness category, and massage therapy sits in the middle. It ranks 10th in affordability out of 17 business types and puts your average across the six most common coverage types comes to about $50 per month, or $597 per year, based on businesses with one to four employees in all 50 states and Washington, D.C.

Your individual policy costs range from $16 to $98 per month depending on coverage type. Our datasets shows workers' comp to be most affordable because getting injured in your profession is unlikely to happen, and if you work solo, you may not need it at all. Cyber insurance costs the most because your practice management software stores client health histories and intake data, which raises your exposure relative to most small businesses.

Treat the figures as benchmarks, not quotes, since your actual premium depends on your specific profile.