Photography is towards the lower end for business insurance costs, like many companies in the arts, entertainment and media category, and ranks 46th overall for affordability out of the 400+ industries I studied. On average the work area sits at $56/mo which is almost half of the national average cost of commercial insurance overall. This is unsurprising given that claims related to bodily injury, property damage and inadequate work which are the most common nationwide, are uncommon, and if they do happen, are settled by the business and client or are too small to make filing with insurance worth it.

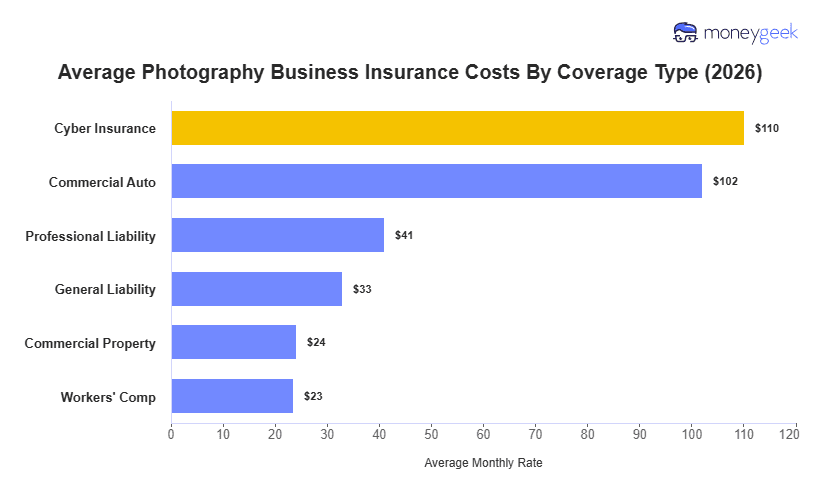

All coverage types sit within the top 100 most affordable for photographers. The one exception here is cyber insurance which is among the opposite end of the spectrum instead at $110/mo. Cyber lands at the top because photographers store substantial volumes of client data: contracts, payment records, and image libraries that create real breach exposure. On the other end, General liability is the cheapest policy for photography businesses due to the lack of risk of property damage, bodily injury associated with taking a picture for someone.