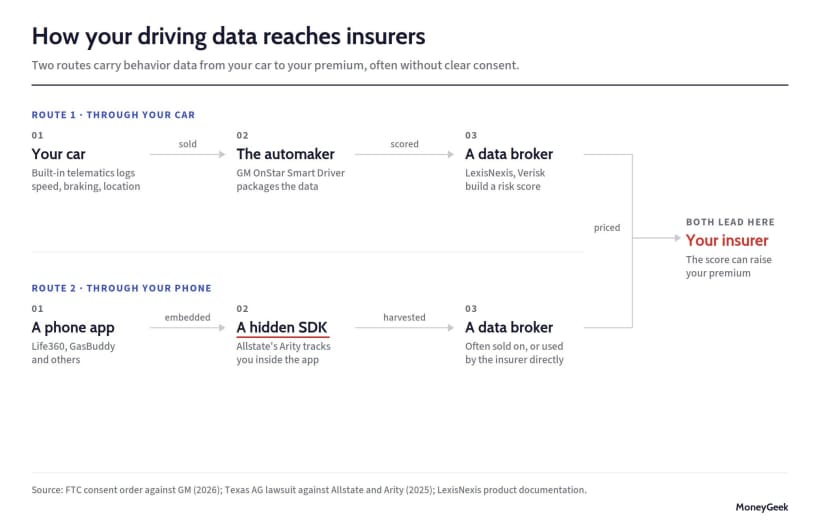

In May 2026, California Attorney General Rob Bonta and partner district attorneys announced a $12.75 million settlement with General Motors, subject to court approval, over allegations that GM sold driving and location data from hundreds of thousands of California drivers to data brokers Verisk Analytics and LexisNexis Risk Solutions. The California DOJ said GM made roughly $20 million nationwide from those sales between 2020 and 2024.

Most new cars sold in the United States now carry telematics systems. According to the FTC's complaint, GM and OnStar collected location data from some drivers as often as every three seconds. GM and Allstate are among the automakers, data brokers and insurers that built a data pipeline. The pipeline routes data from drivers' daily trips to insurers, who use it for pricing. Regulators in California, Texas and at the federal level say the enrollment and disclosure processes used to build that pipeline were unclear or misleading.