When a minor impact pushed the front bumper sensor cover on a friend's 2025 Hyundai Tucson slightly inward, the owner assumed the repair would be simple. The car looked fine. The damage was cosmetic.

The Hyundai dealership had a different read. A service advisor showed where the bent sensor cover had pushed the radar unit toward the ground, which explained why the adaptive cruise control could no longer detect the distance to the car ahead. A body shop would need to replace the bumper, realign the sensor and run a full recalibration. The estimate: more than $1,500.

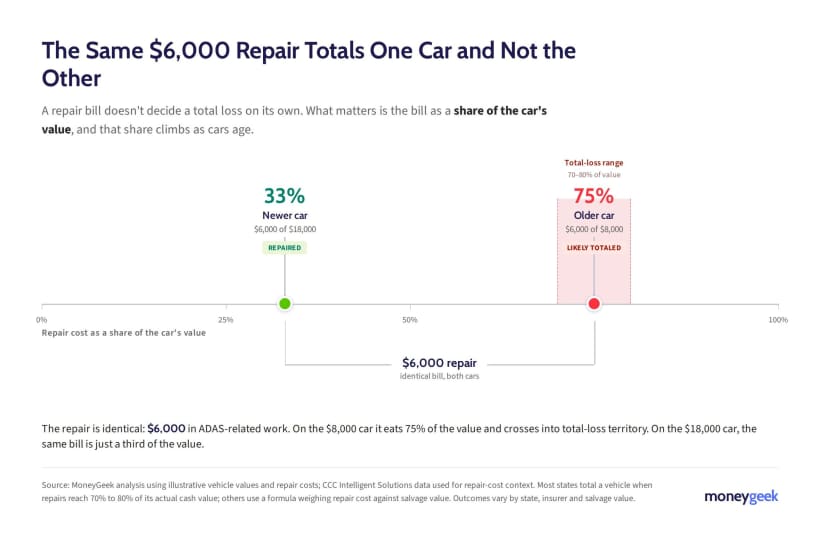

The Tucson was nowhere near a total loss. But the repair showed how advanced driver assistance systems (ADAS) are changing the math after a crash. ADAS encompasses the cameras, radar units and sensors that power automatic emergency braking (AEB), adaptive cruise control and blind spot monitoring. A small hit can now trigger diagnostic scans, sensor alignment and calibration work before a car can safely return to the road.

U.S. crash rates have been falling for years, but a larger share of the crashes that do happen now end in a total loss. CCC Intelligent Solutions' Crash Course 2026 report found that 23.1% of auto physical damage claims it tracked were declared total losses in 2025, up from roughly 17% before 2020. ADAS calibrations now appear on 28.3% of repairable estimates, a 30% increase from 2024 alone. HLDI insurance data on Mazda vehicles shows ADAS-equipped models can reduce crash claim frequency, but the crashes that remain can cost more to fix.