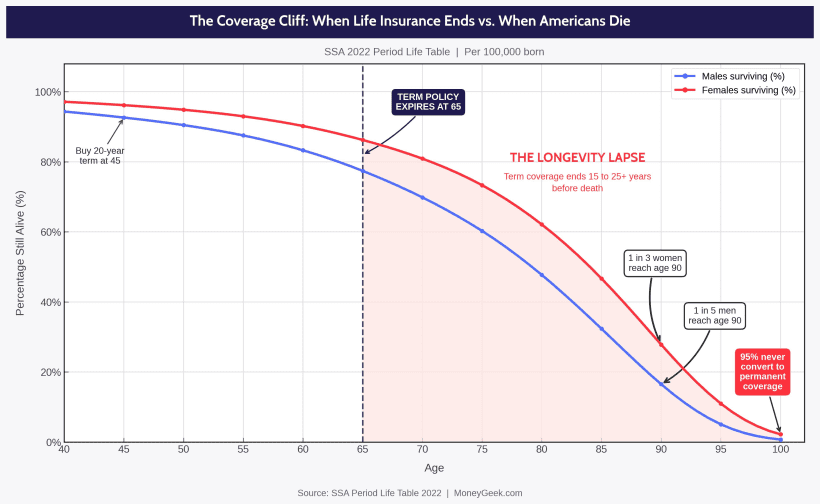

Roughly 4 million Americans turn 65 each year. One in five of the men and one in three of the women will live to 90, all of those years without life insurance, because the 20-year term life policy they bought at 45 expired the day they retired. More than 1 million people from this year's cohort alone will spend up to 25 years uninsured during the years when health costs are highest.

MoneyGeek defines this as the "longevity lapse": the years between when a term policy expires and when the policyholder dies. For the average 65-year-old man, it runs 17.5 years. For the average 65-year-old woman, 20.1 years. For the roughly one in three women who reach 90, it runs 25 years.

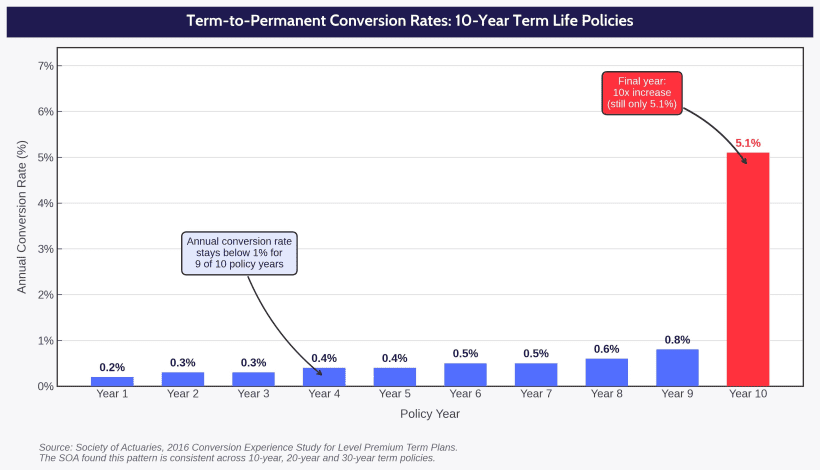

About 95% of term life insurance policyholders never convert to a permanent policy. With annual conversion rates below 1% for most of a policy's life and only about 5% converting even in the final year, most term holders let their coverage end without a backup plan. The SSA's actuarial life tables, the same mortality data the federal government uses to calculate Social Security benefits, put the average policyholder's death 17 to 20 years after their coverage expires.