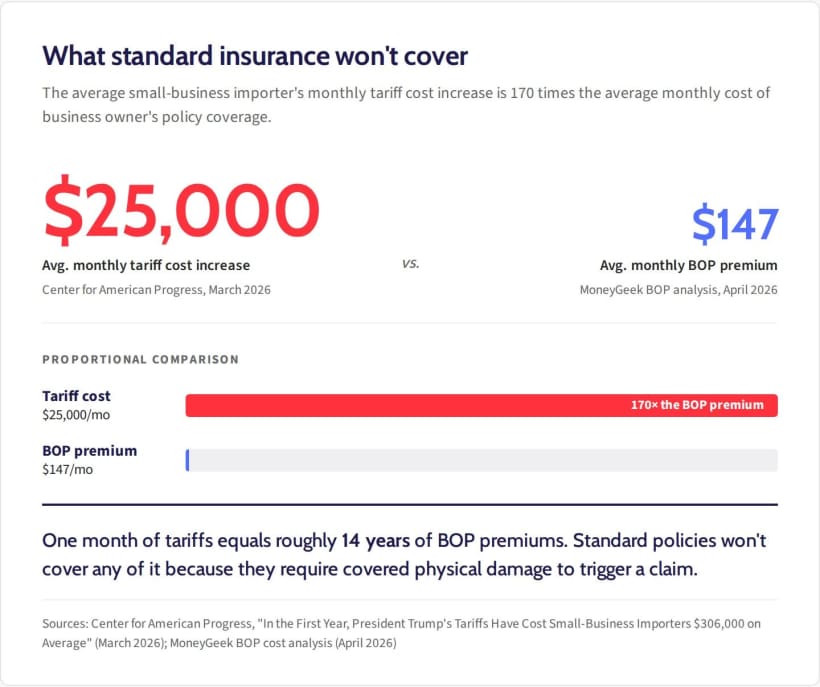

Small businesses that import goods are paying an average of $25,000 more a month in tariff costs than they did a year ago, a March 2026 Center for American Progress report found. That's roughly 170 months, or more than 14 years, of the average monthly business owner's policy premium, based on MoneyGeek's analysis of BOP pricing across 10 national carriers and 79 industries. The smallest firms, those with fewer than 50 employees, paid roughly $175,000 in new tariff costs between March 2025 and February 2026, about $14,600 a month. And the small-business insurance policies most of these businesses carry won't cover a dollar of it.

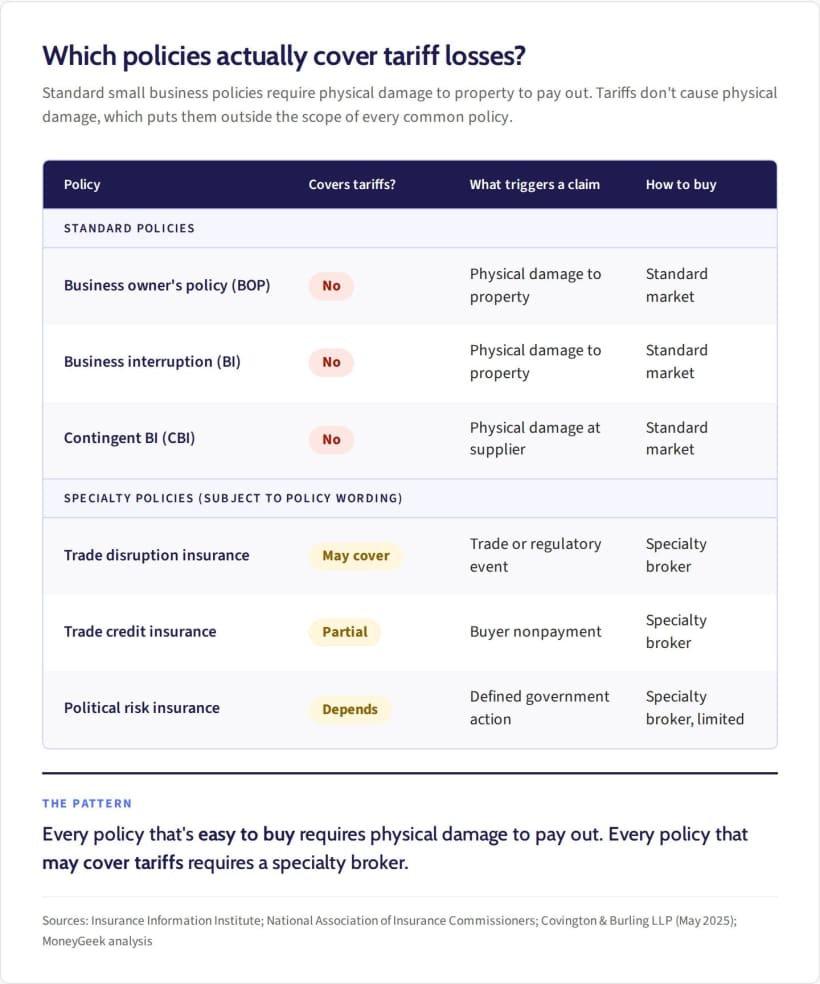

Under a temporary import surcharge that took effect Feb. 24, 2026 (a 10% duty on most imports invoked under Section 122 of the Trade Act of 1974), a non-exempt $50,000 shipment of imported goods adds $5,000 in tariff costs before other duties and fees. For a small-business owner who calls their insurance broker after seeing that line item, the answer from most brokers is the same: standard policies don't cover it.