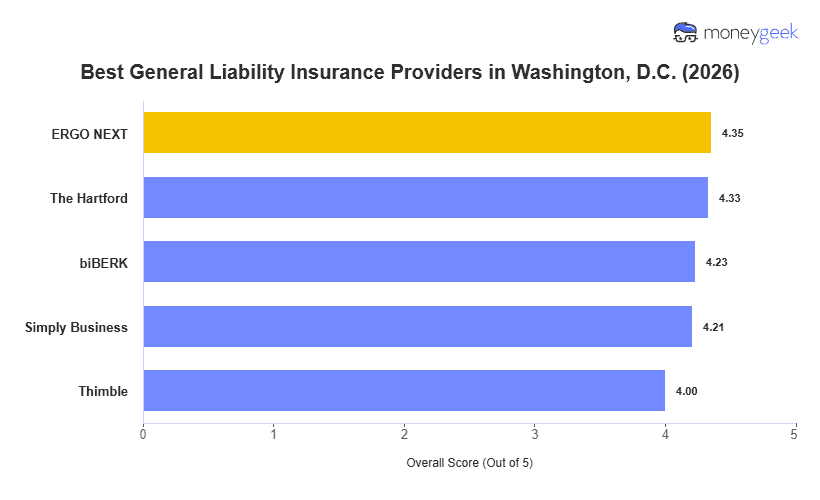

No single insurer is the right fit for every small business in Washington, D.C. These five ranked highest after we analyzed 10 major general liability insurers across 408 business types, using standard limits of $1 million per occurrence and $2 million aggregate. They represent the best and most affordable options operating in the district:

- ERGO NEXT: Best Overall, Best for Hands-On Service Businesses

- The Hartford: Best Cheap General Liability Insurance

- biBERK: Best for Solo and Micro Service Businesses

- Simply Business: Best for Multi-Carrier Quote Comparison

- Thimble: Best for On-Demand and Short-Term Coverage

A Capitol Hill lobbying firm and an Adams Morgan food and beverage operator both carry general liability policies, but what each needs from a provider looks considerably different. Federal contracting requirements, high foot traffic and a concentration of professional services all shape what coverage needs to do in this market. The table below breaks out monthly rates and rankings across all five so you can see where each one lands for your business.