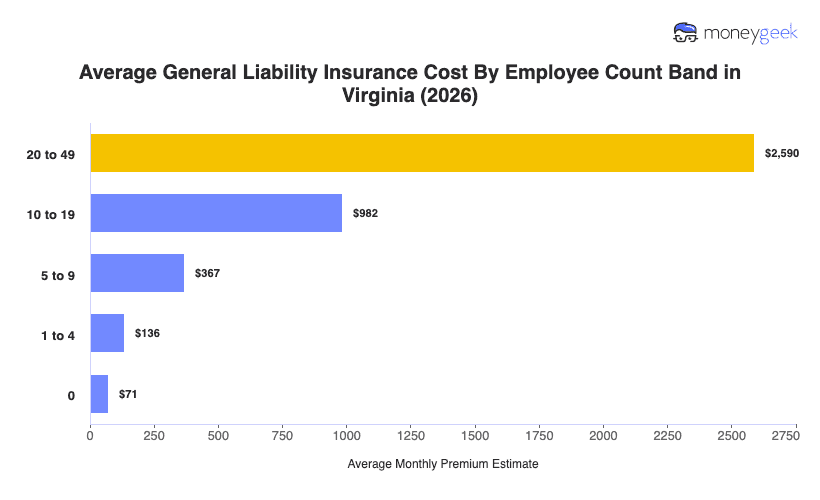

The average cost of general liability insurance in Virginia is $136 per month, or approximately $1,627 annually, for businesses with one to four employees. This benchmark reflects small-business operations and falls 10% above the national average, positioning Virginia 37th nationally for affordability in the upper-middle cost tier.

Virginia's costs fall between its neighbors: West Virginia maintains the nation's most affordable rates at $87 monthly, while Maryland exceeds Virginia at $155 per month. Within the South Atlantic region, most states cluster between $87 and $121 monthly, while Virginia sits above this concentration. This distribution suggests Virginia's regulatory environment or market dynamics contribute to moderately elevated costs, though the benchmark remains a reference point, not a quote as the final pricing shifts with underwriting inputs.

Use the state average to assess where your business likely falls. Costs exceeding this level typically signal higher coverage limits, elevated industry exposure, or larger revenue bases, while costs below reflect lower limits or less-exposed operations. The useful question isn't "Is this expensive?" but rather "Which drivers are moving the number in my case?"