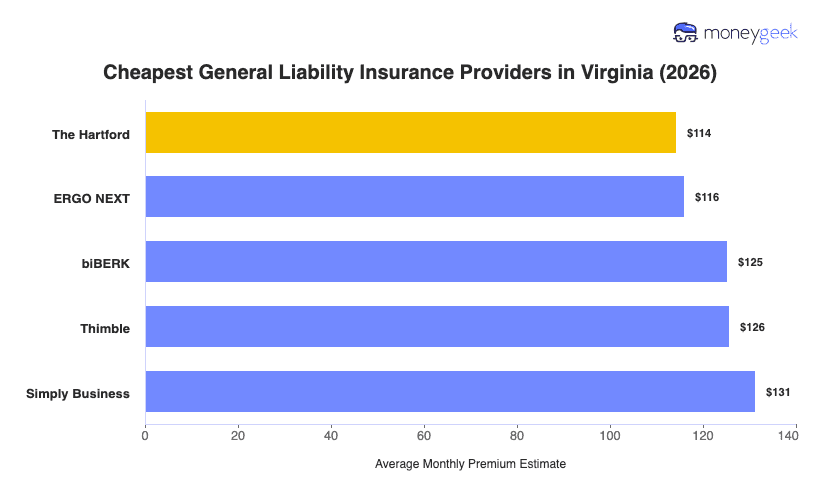

We analyzed rates for $1 million per occurrence/$2 million aggregate coverage across 408 business types in Virginia to identify which insurers offer the most affordable general liability coverage:

- The Hartford: Most affordable for creative professionals and medical practices (wedding photographers, dance studios, chiropractors, dental practices)

- ERGO NEXT: Lowest rates for personal services and construction trades (barber shops, nail salons, HVAC contractors, roofing contractors)

- biBerk: Cheapest for cleaning services and fitness businesses (carpet cleaning, janitorial services, yoga studios, personal training)

[Click Each Provider To Learn More]

Your actual premium depends on factors like annual revenue, employee count and claims history. A Richmond restaurant pays different rates than an Alexandria consulting firm, even with the same coverage limits, so compare quotes from multiple insurers to find the best price for your specific Virginia business.