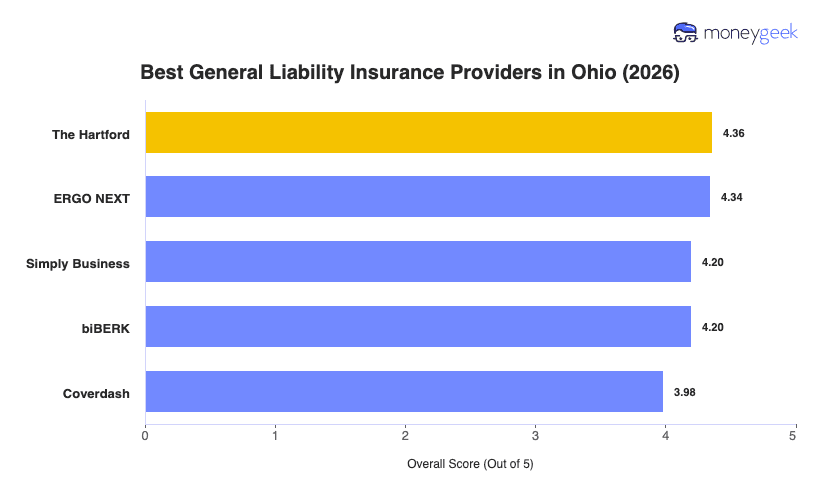

The best general liability insurance companies for Ohio small businesses balance competitive rates with dependable claims handling and flexible coverage options. This group represents the top performers based on MoneyGeek's analysis of 10 major insurers across 25 general industries, evaluating coverage at limits of $1 million per occurrence/$2 million aggregate:

- The Hartford: Best Overall, Best for Service and Care Industries

- ERGO NEXT: Best for Customer Experience

- Simply Business: Best for Multiple Carriers Comparisons

- biBERK: Best for Service Businesses

- Thimble: Best for Seasonal Businesses

This group represents insurers that perform well for Ohio's diverse small business landscape, from seasonal operations dealing with winter weather risks to year-round service providers. What follows is a detailed look at how each stacks up and where their particular strengths make the biggest difference.