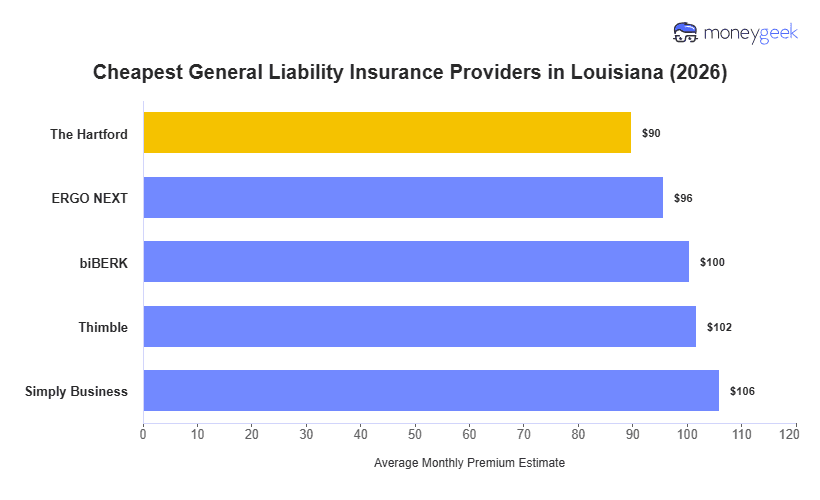

We analyzed over 400 industries across Louisiana to identify the cheapest general liability insurance providers in the state:

- The Hartford: Cheapest for creative professionals, educators and healthcare providers (photography, videography, financial advisors, dentists, physical therapists)

- ERGO NEXT: Most affordable for hands-on trades and customer-facing operations (construction contractors, repair shops, hospitality businesses, transportation services)

- biBERK: Lowest rates for service businesses with physical locations (cleaning services, fitness studios, yoga instructors, real estate agencies, recreation facilities)

>> [Click Each Provider To Learn More]

Your actual rate depends on your industry, revenue, employee count and claims history. Use this as a starting point, then compare quotes built for your specific business.