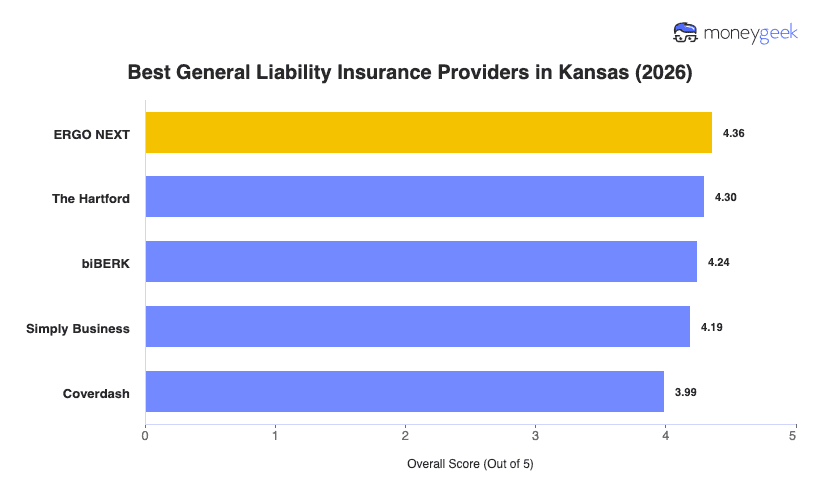

The best and cheapest general liability insurance in Kansas looks different depending on what your business does and how it operates. We analyzed quotes from 10 major insurers at standard limits of $1 million per occurrence and $2 million aggregate across 25 general industries and found these five providers to be the strongest options for Kansas small businesses today:

- ERGO NEXT: Best Overall, Best for Service and Trades Businesses

- The Hartford: Best for Office-Based and Regulated Industries

- biBERK: Best for Client-Facing Service Businesses

- Simply Business: Best for Multi-Carrier Comparison

- Coverdash: Best for Food and Beverage Businesses

A crop-dusting operation outside Dodge City and a barbecue catering company in Kansas City will land in very different places on cost and fit, and the breakdown ahead shows where each provider makes the most sense. The table below shows how each provider ranks and what businesses can expect to pay in Kansas.