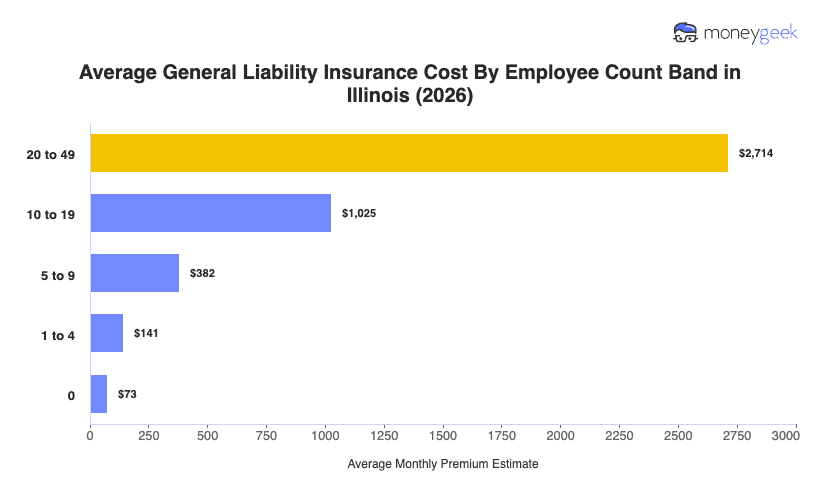

Small businesses with one to four employees, from Chicago marketing agencies to Peoria construction firms, pay $141 monthly or $1,690 annually for general liability coverage based on MoneyGeek's analysis of premium estimates across Illinois. Although the average cost of general liability insurance in Illinois falls 11% lower than the national average, it ranks 39th for affordability. The paradox reveals more about expensive coastal markets inflating the national average than it does about competitive pricing in the Prairie State.

Illinois holds the distinction of being the Midwest's most expensive market for general liability insurance. A Springfield restaurant and a comparable operation in St. Louis show a $36 monthly gap, as the Missouri business pays $105 while the Illinois owner budgets $141. Cross the border into Indiana or Wisconsin and the story stays consistent: Rockford manufacturers pay $33 to $35 more per month than their counterparts in Milwaukee or Fort Wayne. That 23% to 33% regional premium adds up quickly. Over three years, an Illinois landscaping company with four employees spends roughly $1,200 more than the same business operating just across the state line.

Small business owners should use this state average as an initial reference point. Industry claim patterns, your operational risk profile, and prior loss experience determine where you land relative to the $1,690 baseline, not just Illinois's position in regional or national rankings. To get a cost estimate based on your business profile, use the Illinois general liability insurance cost calculator below.