The best general liability insurance companies in Illinois offer more than standard coverage. They understand the risks facing a Naperville contractor, a Chicago food truck operator or a Bloomington retail shop. These five providers rank highest for small businesses across the state, balancing affordable rates with responsive service and policy flexibility that fits how Illinois businesses actually operate.

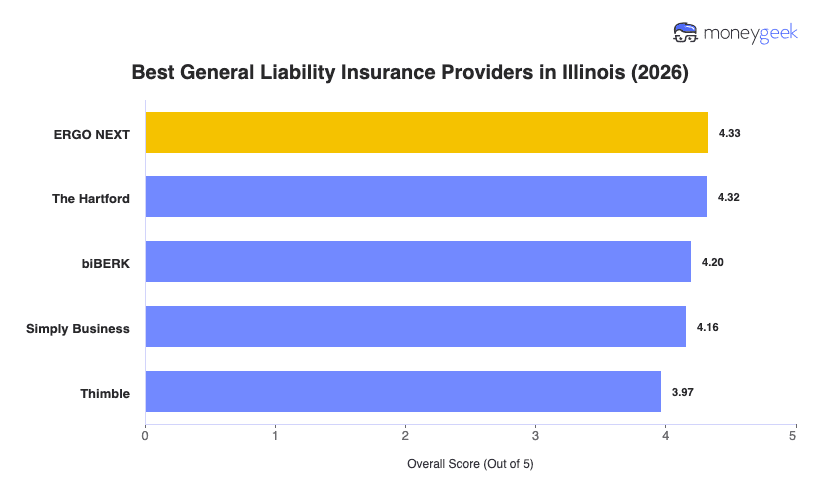

- ERGO NEXT: Best Overall, Best for Customer-Facing Businesses

- The Hartford: Best Cheap General Liability Insurance

- biBERK: Best for Service-Based Businesses with Straightforward GL Needs

- Simply Business: Best for Multi-Carrier Quotes

- Thimble: Best for Flexible Coverage Terms

These companies offer competitive pricing, reliable claims handling and flexible policy options.