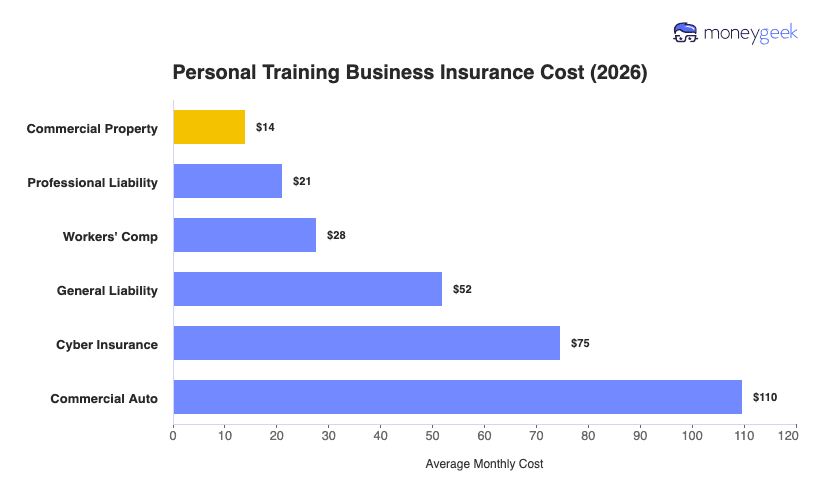

Personal training business insurance averages around $50 per month, or $598 annually, across the six most common coverage types. That figure reflects the average cost of business insurance modeled across 50 states and Washington, D.C., for businesses with one to four employees at standard limits of $1 million per occurrence and $2 million aggregate.

Per-coverage costs range from $14 to $110 per month, with commercial property at the low end because most trainers rent studio space rather than own a building. Commercial auto sits at the high end, though it only applies if you drive to client locations for business.

The table below gives you a starting benchmark, though your actual premium will shift based on your specific profile.