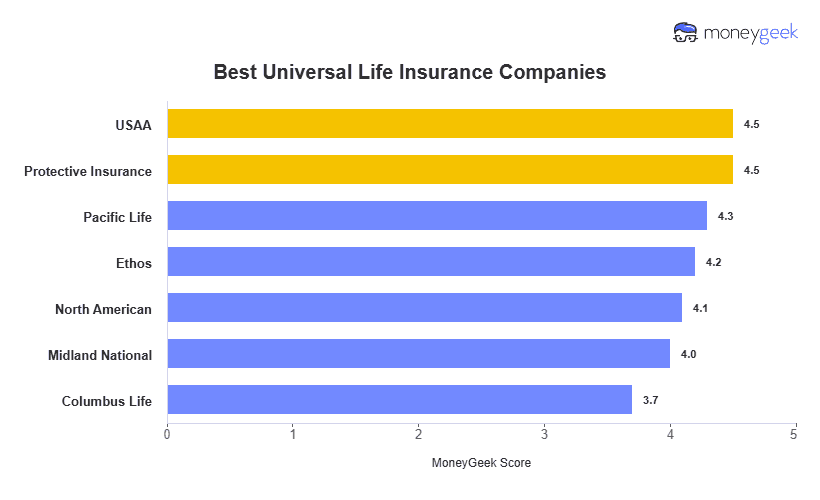

USAA is the best universal life insurance company overall, combining competitive premiums, flexible policy options and strong financial stability. Protective is the most affordable across most age groups, while Ethos has the best indexed universal life options with competitive pricing and fast underwriting.

To find the best universal life insurance companies, we reviewed 20 providers, weighing pricing, policy flexibility, financial strength ratings, cash value growth potential and customer satisfaction. Based on our analysis, the cheapest carrier at age 20 is almost never the cheapest at age 40 or 65. Protective leads on rates across most age group we reviewed, but its NAIC complaint index of 0.21 compares unfavorably to USAA's 0.12. Price gaps also widen sharply after age 60. A 40-year-old woman pays $251 per month with Protective, but at 60, she pays $600. Knowing which carriers price later life stages most favorably changes what "best" means for your situation.