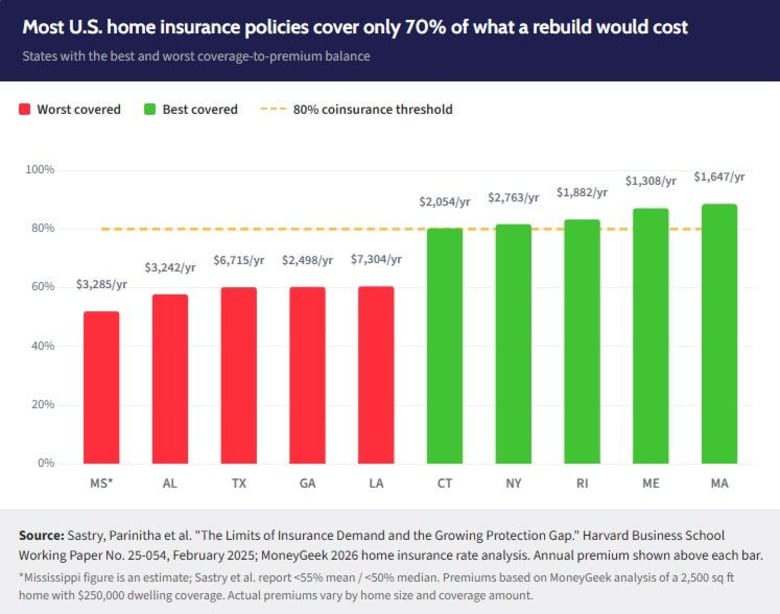

The average U.S. homeowner with a mortgage insures only 70% of what it would cost to rebuild their home from scratch. That's the finding of a Harvard Business School working paper that, for the first time, links roughly 100 million individual mortgage records to insurance policy data at scale. And 70% understates the current problem: the researchers found that average coverage ratios declined from 70% in 2011 to roughly 50% by 2020. The shortfall between what policies pay and what rebuilds cost has widened steadily for more than a decade.

The Marshall Fire put that math into real numbers. It destroyed more than 1,000 homes in Boulder County, Colorado in December 2021. A Federal Reserve Bank of Philadelphia working paper using contract-level data from roughly 5,000 Marshall Fire claims found that 74% of affected homeowners were underinsured, with 36% classified as severely underinsured, meaning their coverage fell below 75% of replacement cost. Colorado's Division of Insurance found that only 8% of homeowners carried guaranteed replacement coverage.