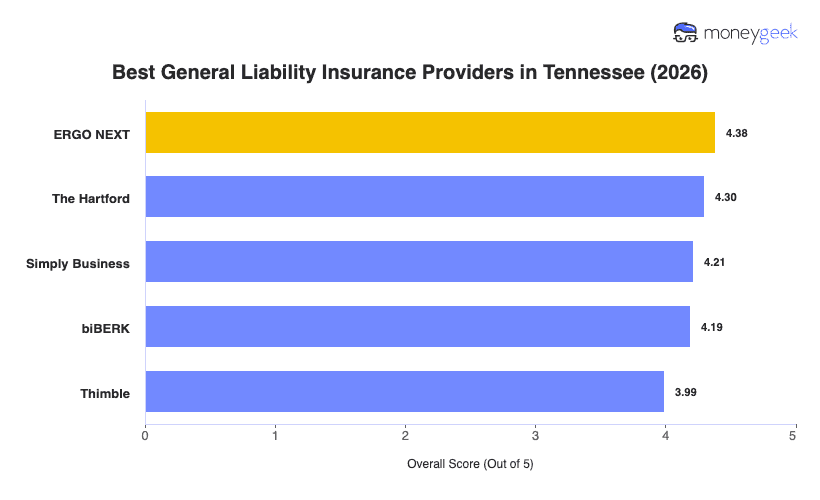

We scored 10 major general liability providers across 25 general industries at $1 million/$2 million coverage limits to find the best and most affordable options in Tennessee. No single insurer works for every business, but these five consistently ranked highest:

- ERGO NEXT: Best Overall, Best for Hands-On and Trade Businesses

- The Hartford: Best for Professional and Institutional Businesses

- Simply Business: Best for Multi-Carrier Comparison

- biBERK: Best for Active and Physical Service Businesses

- Thimble: Best for On-Demand Coverage

The table below compares each provider's rates and rankings, whether you're a construction contractor bidding jobs in Nashville or a retail shop owner in Chattanooga looking to keep costs down.