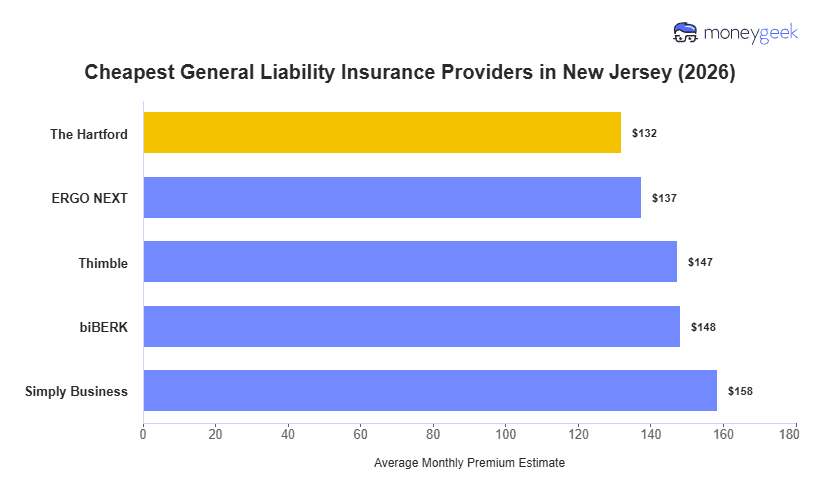

Our analysis of 25 general industries covering over 400 business types showed that these four insurers consistently deliver the most affordable general liability insurance rates for small businesses operating throughout New Jersey.

- The Hartford: Often cheapest for office-based professional services and healthcare practices (photography, IT consulting, dental practices, physical therapy)

- ERGO NEXT: Most affordable for personal services and high-risk construction trades (nail salons, estheticians, roofing contractors, HVAC installers)

- Thimble: Typically has the lowest rates for general construction and engineering services (general contractors, electricians, engineering firms, land surveying)

- biBERK: Generally most affordable for cleaning services and fitness facilities (house cleaning, janitorial services, gyms, yoga studios)

>> [Click each provider to learn more]

Your final premium scales with factors like annual revenue, employee count and the physical risks your work involves. Treat these sweet spots as a starting point, not a guarantee. Compare quotes from multiple insurers to find your actual lowest rate.