State Farm tops Vermont's renters insurance market, scoring 5 out of 5 and ranking first in affordability categories. Auto-Owners comes in second with an overall score of 4.7, excelling in customer experience. Co-operative, Vermont Mutual and Travelers complete the top five.

Best Renters Insurance in Vermont (2026)

Updated: August 1, 2026

Advertising & Editorial Disclosure

Key Takeaways: Vermont Renters Insurance

State Farm is Vermont's best overall renters insurance company, earning a 5 out of 5 MoneyGeek score.

At $94 per year on average, State Farm offers the most affordable renters insurance premiums in Vermont.

Compare quotes from several insurers to find the most competitive rates matching your individual coverage needs.

5 Best Renters Insurance Companies in Vermont

| State Farm | 4.96 | 1 | 2 | 2 |

| Auto-Owners Insurance | 4.65 | 4 | 1 | 5 |

| Co-operative Insurance | 4.61 | 2 | 4 | 1 |

| Vermont Mutual Insurance | 4.43 | 2 | 5 | 4 |

| Travelers | 4.25 | 6 | 3 | 3 |

*Our ratings consider different combinations of coverage levels and renter details to identify the best overall options. Rankings may differ based on your profile.

State Farm

Top Choice for Vermont Renters

MoneyGeek Rating

5.0/ 5

5/5Affordability

4.9/5Customer Experience

4.9/5Coverage

Average Annual Premium

$94Based on our methodology's base profile of a policy with $20K in personal property coverage and $100K in liability coverage with a $500 deductibleAverage Monthly Premium

$8Based on our methodology's base profile of a policy with $20K in personal property coverage and $100K in liability coverage with a $500 deductibleJ.D. Power Renters Insurance Customer Satisfaction Score

685/1,000From the J.D. Power 2025 U.S. Home Insurance Study, which examines customer satisfaction based on responses from 14,511 homeowners and renters. The average renters insurance score is 668/1,000.

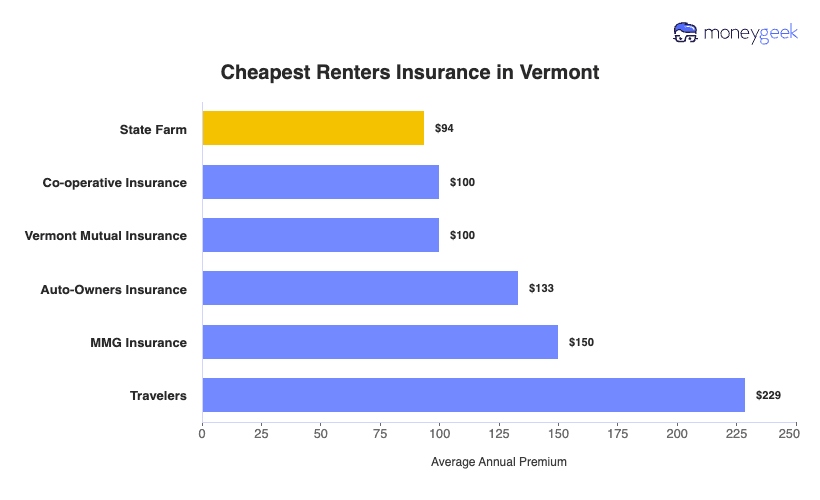

Compare the Cheapest Renters Insurance Companies in Vermont

State Farm charges Vermont's cheapest renters insurance at $94 per year for $20,000 in personal property coverage, $40 below the state average of $134 annually. Co-operative comes in second at $100 per year, while Vermont Mutual costs $100 and is available statewide. All eight cheapest insurers charge below the state average, with rates from $94 to $229 per year, making it easier for renters to find the cheapest renters insurance that fits their budget.

Average Cost of Renters Insurance in Vermont

Vermont renters pay $134 annually for renters insurance on average, $62 under the average cost of renters insurance nationally at $196. These figures are based on a policy with $20,000 in personal property coverage, $100,000 in liability limits and a $500 deductible.

Your actual cost is determined by your coverage limits, deductible choice and location within the state.

| VT | $134 | $-62 |

Do You Need Renters Insurance in Vermont?

Many landlords require renters insurance even though Vermont law doesn't mandate it. Property managers often mandate coverage to protect themselves from liability claims, with many requiring $100,000 or more in liability limits. Your landlord can require coverage as part of your lease agreement. Check your lease before moving in to see if you need a policy.

HOW TO DETERMINE YOUR RENTERS INSURANCE COVERAGE NEEDS

Typical personal property coverage ranges from $20,000 to $50,000 for most renters' belongings. Go through your unit and add up replacement values for electronics, furniture, clothing and other items to calculate your personal property coverage. You'll also want liability limits of $100,000 or more to protect yourself if someone gets injured in your apartment.

How to Find the Best Cheap Renters Insurance in Vermont

Choosing home insurance in Vermont comes down to comparing multiple providers while weighing your budget, coverage requirements and service expectations.

- 1Compare quotes from at least three companies

Premiums differ by $50 or more across companies for identical coverage. Get quotes from both national insurers and regional providers serving Vermont. Burlington and Montpelier residents find the best rates by comparing at least three to five companies. This comparison shopping ensures you're not overpaying for the same level of protection.

- 2Check customer satisfaction ratings and reviews

Low prices aren't worth much if your insurer has poor claims handling. Research J.D. Power ratings and review customer complaints filed with the Vermont Department of Financial Regulation before purchasing. Companies with higher satisfaction scores in areas like Rutland and Essex process claims faster and provide better customer service when you need help most.

- 3Bundle renters and auto insurance

Insurers give 10% to 25% off when you bundle policies together. State Farm and Allstate offer some of the largest bundling discounts available to Vermont residents. This strategy works well for renters in college towns like Brattleboro, where students and young professionals reduce their insurance costs by combining coverage types.

- 4Ask about available discounts

You can get discounts for alarm systems, smoke detectors and staying claims-free for several years. Ask your agent which specific discounts you qualify for to maximize savings. Many Vermont insurers also offer discounts for being a loyal customer, paying your premium annually instead of monthly or completing a home safety course through local programs.

Best Cheap Renters Insurance in Vermont: Bottom Line

Vermont's best renters insurance companies are State Farm, Auto-Owners, Co-operative, Vermont Mutual and Travelers. Get quotes from several companies for the best rates that match your needs. Try the calculator below for personalized quotes depending on your coverage, deductible and credit.

Personalized Vermont Renters Insurance Rates

Get free renters insurance rate estimates for Vermont based on your coverage needs. Rates reflect a profile of renters aged 21 to 64 with no prior claims.

Select Coverage Level

Select Deductible

Select Credit Score

Average Annual Premium—

Select Coverage Level

Average Annual Premium—

Select Deductible

Select Credit Score

Renters Insurance in Vermont: FAQ

Common questions about Vermont renters insurance:

Renters insurance covers only the policyholder and their relatives living in the unit. Your roommate needs their own policy to protect their belongings and get liability coverage. Each roommate should buy separate renters insurance with at least $20,000 in personal property coverage.

Most Vermont renters need $20,000 to $50,000 in personal property coverage and $100,000 in liability protection. Add up replacement costs for your furniture, electronics, clothing and other belongings to calculate your needs. Your landlord may require specific coverage amounts, so check your lease before buying a policy.

Contact your insurer immediately after damage occurs or items get stolen. Document the damage with photos and videos before cleaning up. Provide a list of damaged or stolen items with purchase dates and estimated values. Your insurer will assign a claims adjuster to review your case. Most claims get processed within two to four weeks.

Renters insurance covers temporary housing costs through loss of use coverage if covered damage like fire makes your apartment unlivable. This pays for hotel rooms and restaurant meals while repairs happen. Most policies limit loss of use to 20% to 30% of your personal property coverage amount. Floods and earthquakes aren't covered.

How We Found the Best Cheap Renters Insurance Companies in Vermont

We analyzed Vermont renters insurance companies to identify insurers with low rates and reliable service.

We collected quotes for renters aged 26 to 64 with good credit and no claims history. The profile included $20,000 in personal property coverage, $100,000 in liability protection and a $500 deductible.

Affordability determined 50% of each company's score. Customer satisfaction from industry research made up 40%. Add-on coverage options contributed 10%. Companies with the highest combined scores across all factors made our list of Vermont's best renters insurance providers.

About Mark Fitzpatrick

Mark Fitzpatrick, a licensed Property and Casualty (P&C) Insurance Producer in Connecticut, is MoneyGeek's resident expert in insurance and economics. He has spent nearly a decade covering the market, first at LendingTree and now at MoneyGeek, where he analyzes hundreds of carriers and millions of rates across auto, home, renters, health and life insurance.

His work has appeared in The Washington Post, The New York Times and NPR. He draws on independent cost and consumer experience data, and no insurance company partnerships affect his recommendations.

Mark studied at Boston College before earning a master's in economics and international relations from Johns Hopkins University. Before MoneyGeek, he worked in financial risk management at State Street. He's also a five-time “Jeopardy!” champion.