We analyzed 30 companies and thousands of quotes to find the best whole life insurance providers for 2026, scoring each on affordability, customer experience and coverage options. The most telling finding from our analysis is that USAA has the lowest rates of $504 for women and $513 for men at age 40 but loses its price advantage by age 60. For the older age group, Gerber Life's $1,121 monthly female rate beats USAA's $1,403 rate by $282 per month. That $3,384 annual gap is why our top picks for young adults and seniors aren't the same carrier.

Best Whole Life Insurance Companies (2026)

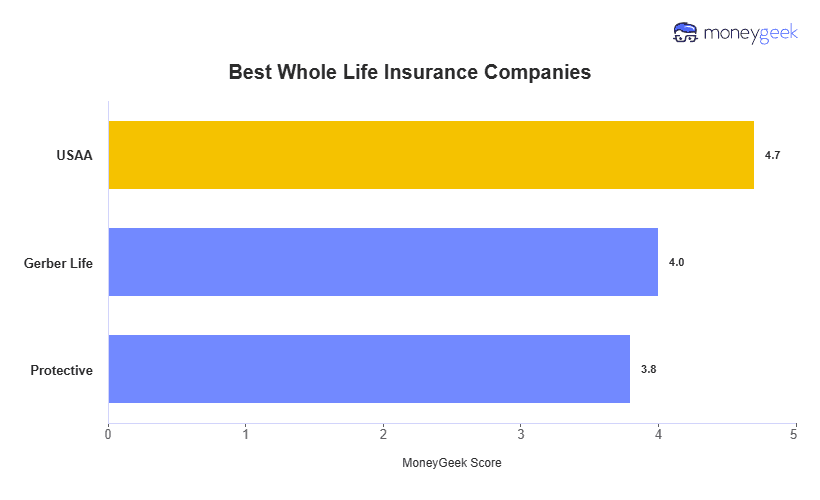

USAA, Gerber Life and Protective are the best whole life insurance companies in 2026.

Compare whole life insurance quotes from top providers.

Select age group

Updated: July 15, 2026

Advertising & Editorial Disclosure

Key Takeaways

Whole life insurance premiums more than double between age 40 and 60. Buy coverage when you're younger to lock in lower rates and save thousands annually.

The best whole life company for a 40-year-old isn't the best for a 60-year-old. USAA has the lowest rates for younger buyers, but Gerber Life is the cheapest option at age 60 by up to $282 per month.

Whole life policies cost 10 to 12 times more per month than a comparable term policy. Permanent coverage makes the most sense for buyers with estate planning goals, lifelong dependents or a guaranteed inheritance strategy.

Cash value grows tax-deferred but builds slowly. Most policyholders don't accumulate meaningful value in the first seven to ten years, and unpaid policy loans reduce the death benefit.

Best Whole Life Insurance Companies

Overall | USAA | $504 (Female), $513 (Male) | 18-85 | $10 million | 4.7 |

Seniors | Gerber Life | $521 (Female), $556 (Male) | 18-80 | $1 million (up to 55), $500,000 (56-80) | 4 |

Young Adults | Protective | $586 (Female), $663 (Male) | 0-80 | $10 million | 3.8 |

* Rates are based on quotes we obtained in our 2026 survey for 40-year-old non-smokers in average health. Costs vary depending on the applicant's age, gender, health rating, smoking status, weight, coverage needs and state regulations. Some states prohibit gender-based pricing. Contact insurers directly for personalized quotes.

MoneyGeek scored whole life insurance carriers on three weighted factors:

Affordability (50%): We gathered quotes online and through agents across different ages and coverage amounts. Lower relative costs score higher.

Customer experience (30%): We reviewed customer forums, NAIC complaint data and industry ratings. Higher scores reflect consistent policyholder satisfaction across policy loans, billing, beneficiary updates and claims.

Coverage options (20%): We assessed dividend participation, rider availability (waiver of premium, long-term care, guaranteed insurability) and customization options. More flexibility scores higher.

Read more in our full Life Insurance Methodology.

USAA

Best Overall

MoneyGeek Rating

4.7/ 5

5/5Affordability

3.9/5Customer Experience

4.9/5Coverage

Average Monthly Rate

$504 (Female), $513 (Male)Ages

18-85Coverage Limit

$10 million

Gerber

Best for Seniors

MoneyGeek Rating

4.0/ 5

4/5Affordability

3.7/5Customer Experience

4.3/5Coverage

Average Monthly Rate

$521 (Female), $556 (Male)Ages

18-80Coverage

$1,000,000

Protective

Best for Young Adults

MoneyGeek Rating

3.8/ 5

4/5Affordability

3.5/5Customer Experience

3.7/5Coverage

Average Monthly Rate

$586 (Female), $663 (Male)Ages

0-80Coverage

$10 million

How Does Whole Life Insurance Work?

Whole life insurance covers you for life and builds cash value you can borrow against. The tradeoff is cost: in MoneyGeek's rate analysis, a 40-year-old woman buying $500,000 in whole life coverage pays about 12 times more a month than a comparable 20-year term policy.

Cash value grows tax-deferred at a guaranteed rate, but most policyholders don't accumulate meaningful value for the first seven to ten years. Permanent coverage is worth the higher premium for estate planning, a dependent with lifelong needs or a guaranteed inheritance. For anyone whose main goal is the lowest-cost death benefit, term coverage costs less.

KEY FEATURES OF WHOLE LIFE INSURANCE

- Lifetime Coverage: The policy lasts your entire life, pays a death benefit when you die and never expires or requires renewal.

- Fixed Premiums: The premium is set at purchase and never increases.

- Cash Value Accumulation: Part of each premium goes into a cash value account that grows at a guaranteed rate. After two to three years, you can withdraw or borrow from it. Unpaid loans reduce the death benefit. Withdrawals may carry surrender charges.

- Guaranteed Death Benefit: Beneficiaries receive a fixed death benefit when you die, which can support estate planning.

- Tax Advantages: Cash value grows tax-deferred. Beneficiaries receive the death benefit tax-free.

Learn more: Benefits of Whole Life Insurance

Types of Whole Life Insurance

Whole life insurance has several types with different premium structures, cash value growth and flexibility. Traditional whole life is the right choice for most buyers because it keeps premiums level for life and avoids the higher upfront costs of limited-pay structures. Limited-pay policies work better if you want coverage paid off before retirement, while single-premium whole life suits high-net-worth buyers who want immediate cash value. Compare types below.

Fixed, level payments for life | Guaranteed growth plus dividends | Long-term stability and predictable budgeting | |

Higher premiums for 10-20 years, then paid-up | Faster cash value accumulation | Those wanting coverage without lifelong payments | |

One lump-sum payment upfront | Immediate cash value growth | High net worth individuals with available capital | |

Lower premiums for 2-3 years, then higher fixed premiums | Guaranteed growth, no cash value contributions during initial period | People who need immediate coverage at lower initial cost and expect higher income later | |

Participating Whole Life | Level premiums with dividend potential | Growth based on insurer performance | Maximizing cash value through dividend reinvestment |

Non-Participating Whole Life | Lower fixed premiums, no dividends | Guaranteed-only growth | Budget-conscious buyers prioritizing death benefit |

How to Choose the Best Whole Life Insurance Company

Choosing the best whole life insurance company isn’t only about cheap prices. Look for long-term value, reliable service and flexible features that match your financial goals. Use this step-by-step guide to compare providers on the factors that matter most.

- 1Check Financial Strength Ratings

Review ratings from AM Best, Standard & Poor's and Moody's. All three of MoneyGeek's top picks hold A+ or higher from AM Best. USAA's A++ is the highest available rating, held by fewer than 2% of rated insurers. A strong rating confirms the carrier can pay claims decades from now.

- 2Understand Dividend Participation

Mutual life insurers share profits with eligible policyholders through annual dividends. Companies like Northwestern Mutual, MassMutual, New York Life and Guardian have paid dividends every year for more than 150 years. If dividends are important to you, compare carriers based on their dividend history, current dividend rate and loan recognition method.

- 3Compare Policy Features and Riders

Common optional life insurance riders include:

- Waiver of Premium: Pauses payments if you become disabled

- Long-Term Care or Chronic Illness Rider: Allows access to part of the death benefit if you need care

- Guaranteed Insurability Rider: Lets you increase coverage later without a medical exam Confirm the carrier has the riders you need before committing.

- 4Evaluate Customer Service and Reputation

Check J.D. Power satisfaction ratings and NAIC complaint data. Read reviews covering claims, billing and policy service. Contact customer support directly to test responsiveness before buying.

- 5Consider No-Exam Policy Availability

Some carriers sell simplified or guaranteed issue policies without a medical exam. These cost more and have lower benefit limits than fully underwritten policies. They fit buyers with health issues or those who need smaller coverage amounts.

- 6Request and Compare Multiple Quotes

Request quotes from at least three carriers. Compare premiums, cash value growth projections, dividend illustrations where applicable, and loan terms. Policy structure and long-term cost matter as much as the opening premium.

How Much Does Whole Life Insurance Cost?

Whole life insurance premiums depend on your age, gender, health and coverage amount. In our analysis, age had the biggest impact on cost. For example, a 40-year-old woman pays $504 to $586 per month for a $500,000 policy, while the same coverage at age 60 costs $1,121 to $1,399 per month. Buying earlier can lock in much lower lifetime premiums.

For comparison, a 20-year, $500,000 term policy for a 40-year-old woman averages $47 per month, about 11 times less than whole life. The higher cost of whole life pays for permanent coverage, guaranteed cash value growth and a death benefit that never expires as long as premiums are paid.

Protective | $290 (F), $336 (M) | $586 (F), $663 (M) | $1,399 (F), $1,612 (M) |

Gerber Life | $307 (F), $356 (M) | $521 (F), $556 (M) | $1,121 (F), $1,286 (M) |

USAA | $311 (F), $319 (M) | $504 (F), $513 (M) | $1,403 (F), $1,431 (M) |

* Rates above are for $500,000 whole life insurance policies for people who don't smoke and have average weight and health.

Estimate Your Whole Life Insurance Cost

Use our free whole life insurance calculator to get a personalized estimate based on your age, gender and coverage level.

Select Age

Select Gender

Select Coverage Level

Select Smoking Status

Average Monthly Rate—

Select Age

Average Monthly Rate—

Select Gender

Select Coverage Level

Select Smoking Status

Bottom Line

The best whole life insurance company depends on your age and long-term goals. For buyers under 50, USAA offers the strongest value, combining the lowest rates at age 40 with an A++ AM Best rating and flexible options like a 20-year pay policy that can be fully funded before retirement.

For seniors 55 and older, Gerber Life is the more affordable option. It has the lowest rates at age 60, accepts applicants up to age 80 and doesn't require a medical exam, though coverage is capped at $500,000 after 55 years old.

Protective is most competitive for younger buyers, especially people ages 20 to 35 who want to build decades of cash value growth. It's the cheapest provider for people in their 20s, but its pricing advantage fades by age 40. For applicants with serious health conditions, USAA and Gerber Life both offer guaranteed acceptance options, but Protective doesn't.

Compare quotes from at least three providers before purchasing a policy to get the best rate.

Frequently Asked Questions (FAQs)

Find the answers to some of the most common questions you have about whole life insurance:

Part of each premium goes into a cash value account that grows at a guaranteed rate. You can borrow against or withdraw this money, though doing so reduces your death benefit. The cash value grows tax-deferred over time.

Whole life insurance is worth the higher premium if you need lifelong coverage, want guaranteed cash value growth or have estate planning goals. If you only need temporary coverage or are on a tight budget, term life insurance is the more cost-efficient option.

Term life insurance is more affordable and offers coverage for a set period, making it a good choice for those with temporary financial obligations or a limited budget.

Whole life offers permanent coverage and includes a savings component that builds cash value over time. It’s a good choice for those who want lifelong coverage and the ability to accumulate savings that you can borrow against or use to pay premiums.

Learn more: Term vs. Whole Life Insurance

You can cancel anytime and receive the cash surrender value, which is your cash value minus surrender charges. These charges decrease over time and may disappear entirely after 10 to 20 years, depending on your policy. Try alternatives like reducing coverage or taking policy loans first.

Yes, you can borrow against your whole life insurance policy's cash value once it accumulates. These loans don't usually require credit checks or repayment schedules. However, unpaid loans plus interest reduce your death benefit and could cause policy lapse if the balance exceeds your cash value.

Whole life insurance isn't ideal as an investment. It provides lifelong coverage with cash value growth, but returns tend to lag behind stocks, bonds or index funds. The high premiums and fees make it better suited as insurance protection rather than wealth building.

Learn more: Is Whole Life Insurance a Good Investment?

Most term life policies include a conversion rider that lets you convert to whole life without a medical exam, usually within the first 10 to 20 years.

Premiums at conversion are higher based on your current age, but the conversion locks in your insurability regardless of health changes since the original purchase.

Whole life insurance dividends are annual payments that participating policies can receive when an insurer earns more than it projected from investments, policyholder mortality and administrative expenses. Dividends aren't guaranteed, but the largest mutual life insurers have paid them every year for over 150 years. USAA, Gerber Life and Protective don't pay dividends because they're stock companies rather than mutual companies.

Related Articles

About Patrick Bryant

Patrick Bryant is the Vertical Lead for Life and Health Insurance at MoneyGeek, where he researches insurance products, writes consumer guides and maintains the scoring methodologies behind our provider comparisons. He analyzed more than 50 life insurance carriers across multiple policy types, collecting thousands of quotes nationwide to evaluate rates, coverage options and underwriting factors. His methodologies are reviewed quarterly to reflect current market conditions and carrier data.