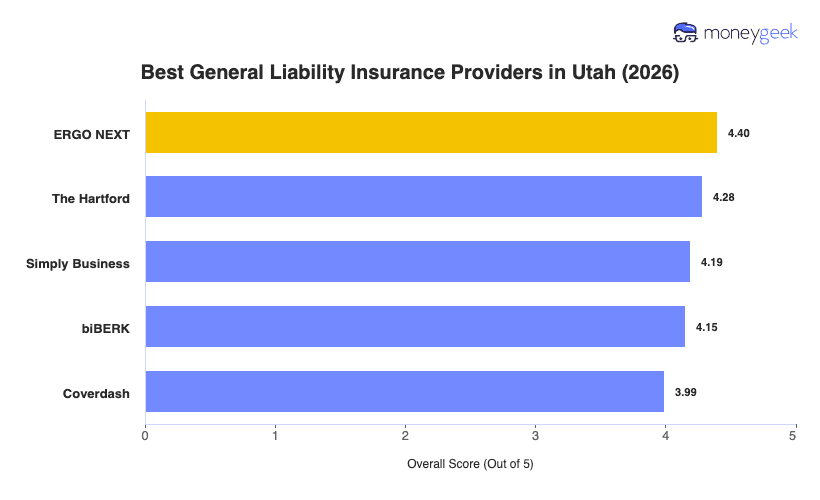

No single general liability insurer fits every Utah business, but these five providers rank highest across the state for balancing cost, service quality and coverage strength, whether you run a one-person operation or manage a growing team. MoneyGeek analyzed 10 major insurers across 25 general industries to identify the best general liability insurance companies for Utah small businesses.

- ERGO NEXT: Best Overall, Best for Digital-First Buyers

- The Hartford: Best for Professional Services

- Simply Business: Best for Carrier Choice

- biBERK: Best for Personal Services

- Thimble: Best for Flexible-Term Coverage

These five insurers handle everything from slip-and-fall claims at Provo retail shops to equipment damage allegations at Ogden construction sites. The detailed profiles below break down pricing, coverage options and where each provider excels across Utah's diverse business landscape.