Full coverage motorcycle insurance is the industry term for a policy that includes state-required liability protection and optional physical damage coverage for your bike. This type of coverage combines liability, collision, and comprehensive coverage into a single policy, creating complete financial security compared to minimum coverage policies that include only state-mandated liability.

Full Coverage Motorcycle Insurance

Updated: June 11, 2026

Advertising & Editorial Disclosure

Key Takeaways

Full coverage motorcycle insurance covers the bike through collision and comprehensive coverage but excludes medical bills. Adding medical payments coverage protects against hospital costs that typically range from $15,000 to $150,000.

Full motorcycle insurance coverage averages $302 to $800 per year, depending on the carrier, with Harley-Davidson offering the lowest rates, per MoneyGeek's analysis.

Full coverage motorcycle insurance is worth the cost for bikes valued above $5,000 or when replacement costs would strain your savings. For lower-value bikes, liability-only coverage costs less and self-insuring the physical damage risk is a reasonable alternative.

What Is Full Coverage Motorcycle Insurance?

What Does Full Coverage Motorcycle Insurance Cover?

Full coverage motorcycle insurance protects you in three main situations: when you injure someone or damage their property, when your bike needs repairs after a crash and when it’s damaged while parked because of theft or weather.

Each part of the policy covers a different risk and comes with its own claim rules, deductibles, and limits, so it helps to review these details before choosing your plan.

Liability Coverage

Motorcycle liability insurance provides coverage into two components. Bodily injury liability covers others' medical expenses, lost wages, and pain and suffering when you injure them in a crash. Property damage liability pays for vehicle repairs, building damage, and property destruction you cause. Your insurer pays these claims to your liability limits, protecting your personal assets from lawsuits after at-fault accidents.

Most states require liability coverage as minimum motorcycle insurance. However, state minimums often provide insufficient protection. A $25,000 bodily injury limit won't cover serious injury costs exceeding $100,000. Consider carrying $100,000/$300,000 in bodily injury and $50,000 in property damage limits for adequate protection, especially if you have assets worth protecting, such as a home, savings, or retirement accounts.

Collision Coverage

Motorcycle collision coverage pays for repairs after accidents with vehicles or stationary objects, regardless of fault. The deductible applies first; the insurer covers remaining repair costs up to the bike's actual cash value. Typical deductibles range from $250 to $1,000.

Collision coverage applies when a rider rear-ends another vehicle, sideswipes a car while changing lanes, or hits a guardrail. Without collision coverage, all accident repair costs come out of pocket. Moderate damage typically costs $3,000 to $10,000, which can drain savings or require financing on a bike that may still carry a loan balance.

Collision coverage is worth carrying on financed bikes or any bike worth more than the rider could afford to replace from savings.

Comprehensive Coverage

Comprehensive motorcycle coverage protects your bike against non-collision perils: theft, vandalism, fire, flood, hail, falling objects, and animal strikes. Theft is the most common comprehensive claim. Your insurer pays for repair or replacement costs up to actual cash value, minus your deductible.

What Does Full Coverage Motorcycle Insurance Not Cover?

Full coverage doesn't cover your injuries, a critical gap many riders overlook. You'll need to add medical payments coverage or personal injury protection to cover your hospital bills, rehabilitation costs, and lost wages after accidents. Some states mandate PIP, but many don't. The gaps below are the most common surprises riders encounter when filing claims, from discovering their medical bills aren't covered to learning their custom parts have no protection.

Your Own Medical Expenses

Full coverage does not pay for hospital bills, rehabilitation costs or lost wages after an accident. Liability, collision and comprehensive coverage protect other people and the bike, not the rider. Medical payments coverage with limits from $1,000 to $10,000, or personal injury protection (PIP) for broader coverage, including lost wages, fills that gap.

The National Highway Traffic Safety Administration reports that 80% of motorcycle crashes result in injuries. Without medical coverage, treatment costs of $15,000 to $150,000 come out of pocket, from savings or through health insurance that typically carries its own deductibles and copays. MedPay starts at $5 to $15 per year for every $5,000 in coverage.

Custom Parts and Aftermarket Accessories

Standard collision and comprehensive coverage excludes custom exhaust systems, upgraded seats, paint jobs, saddlebags, and aftermarket equipment. Your $2,000 custom exhaust and $1,500 upgraded suspension won't be covered unless you add custom parts and equipment coverage with limits typically ranging from $3,000 to $10,000.

Progressive automatically includes $3,000 in accessory coverage with full coverage. Other insurers require you to purchase this separately. Comprehensive coverage without this endorsement will only reimburse your bike's stock value, not the $5,000-$15,000 you've invested in customizations.

Custom bikes often require modifications of over $10,000. Without custom equipment coverage, you'll lose this entire investment after total-loss crashes or theft. Custom parts coverage costs just $50-$150 annually, a small price to protect significant investments.

Mechanical Breakdown and Normal Wear

Full coverage doesn't pay for engine failures, transmission problems, or maintenance-related repairs. Motorcycle and comprehensive collision coverage only cover sudden, unexpected damage from covered perils, not age-related mechanical failures or neglected maintenance issues. You would have to purchase separate mechanical breakdown insurance to get this level of protection.

Roadside Assistance and Towing

Full coverage motorcycle insurance doesn't include towing or roadside assistance unless you add it separately. Without this $5- $15 annual add-on, you'll pay $75-$200 out-of-pocket for tow truck services after breakdowns.

Racing and Commercial Use

Track days, competitive events, food delivery work, and ride-sharing void your full coverage policy. Crashes during these activities will result in denied claims. You'll need specialized track insurance or commercial motorcycle insurance for these uses.

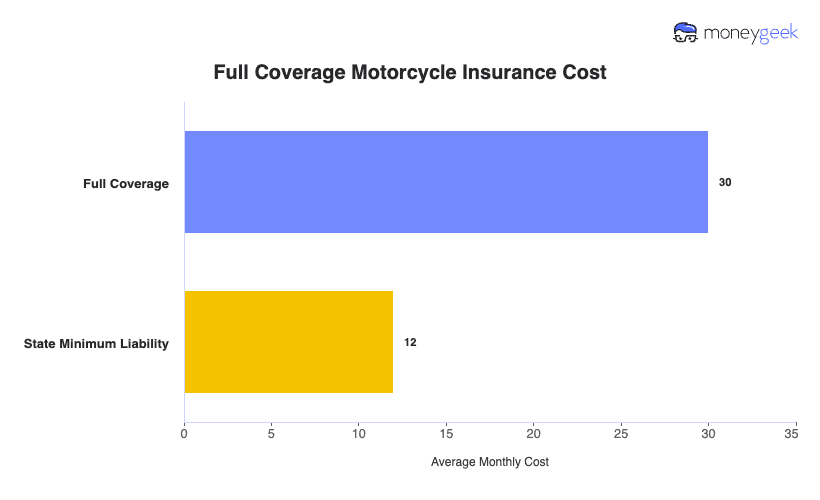

Full Coverage Motorcycle Insurance Cost

Full coverage motorcycle insurance costs $364 annually compared to $141 for state minimum liability, a difference of $223 per year. Whether this premium increase is worth paying depends entirely on your bike's value and financial capacity to replace it.

| Full Coverage | $30 | $364 | $10 | $103 |

| State Minimum Liability | $12 | $141 | $4 | $49 |

The national average above establishes a baseline for full coverage motorcycle insurance costs. The lowest and maximum monthly costs show the typical range riders pay. In the following sections, we will show how your age impacts your premium as you gain riding experience, which insurers offer the cheapest full coverage motorcycle insurance, and how your location affects your premiums.

Average Full Coverage Motorcycle insurance cost by Age

Full coverage motorcycle insurance costs $1,146 annually for 16-year-olds, $907 for 21-year-olds, $632 for 25-year-olds, and $364 for 40-year-olds. Your age creates the single most significant impact on your premium, with rates dropping by nearly 70% from your teen years to age 40. The steepest rate drops occur between ages 21 and 30, where premiums fall by almost $500 annually.

Average Full Coverage Motorcycle Insurance by Company

Harley-Davidson Insurance averages $302 annually, 57% below the national average. It is followed by Dairyland at $544, 23% below average and GEICO at $580, 18% below average.

This means identical full coverage motorcycle insurance costs anywhere from $302 to $800 annually, depending on which insurer you choose. Compare the average cost of motorcycle insurance below to see which companies offer the most affordable rates.

| Harley | $25 | $302 | -57% |

| Dairyland | $45 | $544 | -23% |

| Geico | $48 | $580 | -18% |

| Progressive | $51 | $612 | -14% |

| Nationwide | $85 | $1,025 | 45% |

| Markel | $96 | $1,157 | 63% |

Average Full Coverage Motorcycle Cost by State

Where you live has a bigger impact on your premium than any other factor, with an 835% gap between the cheapest and most expensive states. Southern states such as Alabama and Texas tend to have lower rates because of fewer people and lower theft risks.

In contrast, urban states with longer riding seasons, including Arizona and Michigan, often charge 84% to 164% above the national average.

| Alabama | $23 | $273 | -62% |

| Alaska | $17 | $200 | -72% |

| Arizona | $156 | $1,871 | 164% |

| Arkansas | $34 | $411 | -42% |

| California | $46 | $553 | -22% |

| Colorado | $27 | $321 | -55% |

| Connecticut | $29 | $349 | -51% |

| Delaware | $39 | $466 | -34% |

| Florida | $119 | $1,431 | 102% |

| Georgia | $33 | $399 | -44% |

| Hawaii | $29 | $351 | -50% |

| Idaho | $29 | $352 | -50% |

| Illinois | $35 | $417 | -41% |

| Indiana | $37 | $449 | -37% |

| Iowa | $20 | $238 | -66% |

| Kansas | $19 | $231 | -67% |

| Kentucky | $38 | $456 | -36% |

| Louisiana | $38 | $459 | -35% |

| Maine | $27 | $319 | -55% |

| Maryland | $31 | $373 | -47% |

| Massachusetts | $28 | $335 | -53% |

| Michigan | $38 | $456 | -36% |

| Minnesota | $19 | $224 | -68% |

| Mississippi | $44 | $530 | -25% |

| Missouri | $41 | $496 | -30% |

| Montana | $14 | $170 | -76% |

| Nebraska | $29 | $344 | -52% |

| Nevada | $40 | $485 | -32% |

| New Hampshire | $30 | $358 | -49% |

| New Jersey | $46 | $557 | -21% |

| New Mexico | $35 | $418 | -41% |

| New York | $23 | $282 | -60% |

| North Carolina | $31 | $377 | -47% |

| North Dakota | $19 | $222 | -69% |

| Ohio | $26 | $315 | -56% |

| Oklahoma | $27 | $319 | -55% |

| Oregon | $127 | $1,522 | 115% |

| Pennsylvania | $24 | $284 | -60% |

| Rhode Island | $47 | $565 | -20% |

| South Carolina | $30 | $360 | -49% |

| South Dakota | $20 | $237 | -67% |

| Tennessee | $34 | $411 | -42% |

| Texas | $158 | $1,891 | 167% |

| Utah | $108 | $1,290 | 82% |

| Vermont | $28 | $337 | -52% |

| Virginia | $34 | $413 | -42% |

| Washington | $24 | $288 | -59% |

| West Virginia | $41 | $490 | -31% |

| Wisconsin | $24 | $291 | -59% |

| Wyoming | $21 | $247 | -65% |

Factors That Affect The Cost Full Coverage Motorcycle Insurance

Full coverage motorcycle premiums are based on several rating factors. Some, including age and location, are outside your control. Others create room to lower costs. The factors below are listed by impact level, from those that affect premiums most to smaller discounts that can be combined for additional savings.

Your Age and Riding Experience

Younger riders pay higher premiums because they statistically file more claims. A 16-year-old pays about 215% more than a 40-year-old for the same coverage, based on MoneyGeek's cost analysis. Premiums decrease gradually as riders age and maintain a claim-free record, with the largest drops occurring between ages 21 and 30.

Your Driving Record

Traffic violations and at-fault accidents raise motorcycle insurance premiums for three to five years after each incident. Speeding tickets typically increase premiums by 10% to 25%; DUI convictions often double or triple rates.

Insurers rely heavily on driving history to estimate future claims. A clean record is one of the most effective ways to maintain lower premiums over time.

Your Motorcycle's Value and Type

High-value bikes carry higher insurance costs because replacement after theft or a total-loss crash costs more. Collision and comprehensive premiums are based on the bike's actual cash value.

Sport bikes and supersport models carry the highest rates due to their association with high-speed crashes. Cruisers and touring bikes typically cost less to insure.

Your Location

Where you live and where you store your bike affect your rates more than any other factor. Urban areas with high theft levels lead to much higher comprehensive costs.

States with more accidents and expensive medical care push liability and collision premiums higher as well. As shown in the state cost table above, premiums differ by as much as 835% between the cheapest and most expensive states.

Your Coverage Limits and Deductibles

Higher liability limits raise your premium because the insurer takes on more financial risk, but the increase is usually small compared to the extra protection you get. Your deductible choice has a much bigger impact on cost. Moving from a $250 deductible to $1,000 lowers your collision and comprehensive premiums by 30% to 40%.

Your Credit Score

Most states allow insurers to use credit-based insurance scores when calculating premiums. Riders with excellent credit pay less than those with poor credit, even with identical riding records. Insurers correlate credit scores with claim frequency. California, Hawaii, Massachusetts and Michigan prohibit this practice.

Your Annual Mileage

Riders who travel fewer miles annually carry lower accident risk and may qualify for low-mileage discounts. Riders covering under 5,000 miles per year should inform their insurer; many carriers offer 5% to 15% discounts for recreational riders compared to daily commuters covering 10,000 or more miles per year.

Safety Features and Anti-Theft Devices

Anti-theft systems reduce comprehensive coverage costs by making a bike harder to steal. Anti-lock brakes (ABS) can reduce premiums by 5% to 10% because ABS-equipped bikes have fewer crashes. Some insurers offer discounts for additional safety equipment such as airbag vests or GPS tracking systems.

Multi-Policy Bundling

Bundling motorcycle insurance with auto or home coverage generates 15% to 25% discounts from most insurers. This is one of the largest available discounts and requires no change to riding behavior or equipment.

Safety Course Completion

Completing Motorcycle Safety Foundation courses or state-approved rider training reduces premiums by 5% to 15% with most insurers. These courses typically cost $150 to $350 but generate premium savings for three or more years, offsetting the course cost while improving riding skills and crash avoidance.

Storage Location

Keeping your bike in a locked garage instead of on the street lowers your comprehensive premium because it reduces theft and weather risks. Many insurers offer a 5% to 10% discount for garaged bikes compared with those left on the street.

Is Full Coverage Motorcycle Insurance Worth It?

Deciding between full coverage and liability-only comes down to your bike’s value, how you use it and whether you could shoulder a total loss out of pocket. Full coverage costs about $223 more per year, but that extra amount protects you from losses of $3,000 to $25,000 if your bike is stolen or damaged in a crash.

When Getting Full Coverage Motorcycle Insurance Makes Sense

Full coverage is worth carrying on motorcycles valued above $5,000. Without it, repairs or replacement come entirely out of pocket. A stolen or totaled $10,000 bike with liability-only coverage leaves the owner absorbing the full loss.

Riders without substantial emergency savings should also consider full coverage. Repairs on a $3,000 to $5,000 bike can run $2,000 to $4,000 after an accident, which can exhaust an emergency fund or require high-interest financing.

Lenders require full coverage on financed or leased motorcycles to protect against loss on a bike that still carries a loan balance. Riders who depend on their motorcycle as primary transportation benefit from full coverage because repairs are covered rather than paid out of pocket, reducing time off the road.

When Liability-Only Coverage Makes Sense

Liability-only coverage works well for bikes worth less than $2,000. Premium savings typically equal the bike's value within two to three years. For bikes valued between $2,000 and $5,000, divide the bike's value by $223; if the result is three years or less, liability-only coverage and self-insuring the physical damage risk is the more cost-effective option.

Riders who log fewer than 1,000 miles per year and store their bikes in a garage most of the time carry a lower accident risk. Liability-only coverage meets legal requirements at a lower cost, though comprehensive coverage still protects garaged bikes from theft. Riders more concerned about theft than crash damage can keep comprehensive and drop collision.

Riders with $10,000 or more in accessible emergency savings can absorb a total loss without financial disruption. Liability-only insurance reduces costs while meeting legal requirements, and premium savings over several years often exceed the cost of unlikely claims.

How to Get Full Coverage Motorcycle Insurance

Comparing quotes from multiple insurers before buying full coverage motorcycle insurance saves most riders $200 to $500 per year for the same protection.

- 1Gather Your Motorcycle Information

You need your bike's year, make, model and VIN to get accurate quotes. Have your current odometer reading ready since annual mileage affects your premium. If you've added custom parts, document their value with receipts or appraisals. Standard collision and comprehensive coverage excludes aftermarket modifications.

- 2Collect Your Personal Information

Insurers need your date of birth, driver's license number and motorcycle license date. List any traffic violations or at-fault accidents from the past three to five years. If you've completed motorcycle safety courses, have your certificates ready. Most insurers offer 5% to 15% discounts for approved training.

- 3Decide Your Coverage Needs

Ask one question: Can you afford to replace your bike if it's stolen or totaled? If a $5,000 to $15,000 loss would cause financial hardship, you need full coverage with collision and comprehensive. If your bike is worth less than $3,000 and you have strong emergency savings, liability-only coverage costs less.

Choose liability limits that protect your assets. If you own a home or have savings and retirement accounts, choose $100,000/$300,000 bodily injury and $50,000 property damage. State minimums of $25,000/$50,000 won't cover serious injury costs, which leaves you personally liable for the difference.

- 4Request Quotes From Multiple Insurers

Contact at least three insurers. Premiums vary by hundreds of dollars per year between companies. The cheapest full coverage motorcycle insurance costs 57% less than the average in MoneyGeek's analysis.

Request quotes from Harley-Davidson Insurance (if you ride a Harley), Dairyland, GEICO, Progressive and Nationwide. Get quotes online, call agents directly or work with an independent agent who can quote multiple companies at once.

- 5Compare Coverage Options and Prices

Check that each quote uses the same coverage limits and deductibles. Confirm that optional coverages match across all quotes, including medical payments coverage, rental reimbursement, roadside assistance and custom parts protection.

Don't choose based on price alone. Check each insurer's AM Best financial strength rating and state complaint ratios to confirm they pay claims reliably.

- 6Ask About Available Discount

Ask about all available discounts: multi-policy bundling (15% to 25%), motorcycle safety course completion (5% to 15%), anti-theft devices, anti-lock brakes, low annual mileage, good credit and mature rider discounts. Many insurers offer 10 or more discounts that can be combined. A $364 full coverage policy often drops to $250 to $300 with multiple discounts applied.

- 7Purchase Your Policy

Full coverage motorcycle insurance can be purchased online or by phone. You'll pay your first month's premium or a down payment on a six-month or annual policy. Paying in full typically saves 5% to 10% compared to monthly installments. Coverage starts immediately after payment, and proof of insurance arrives by email within minutes..

- 8Review Your Policy Documents

Check your policy documents to confirm that coverage limits, deductibles and endorsements match what you purchased. Verify that custom parts coverage, medical payments coverage and other optional protections appear on your declarations page. Confirm your bike's VIN, address and lienholder information are correct. Contact your insurer right away if you find errors; mistakes can lead to claim denials.

- 9Maintain Continuous Coverage

Set up automatic payments or calendar reminders to pay premiums on time. A lapse in coverage raises future rates and leaves you financially exposed. Most states require continuous insurance for registered motorcycles. A lapse can result in license suspension, registration revocation and reinstatement fees of $50 to $500, depending on your state.

Comprehensive Motorcycle Insurance: Bottom Line

Full coverage motorcycle insurance combines liability, collision and comprehensive coverage into one policy, protecting both your legal liability and your bike's physical value. The right choice between full coverage and liability-only comes down to one question: can you afford to replace your bike from savings if it's stolen or totaled? If not, full coverage is the stronger option. If you can absorb that loss without financial hardship, liability-only costs less.

Premiums vary by age, location and insurer. You control several factors that reduce costs: comparing quotes from multiple companies, bundling with other policies, completing safety courses and raising your deductible.

Full coverage does not cover everything. Medical expenses, custom parts and mechanical failures each require separate coverage. Compare quotes to find the right balance of protection and cost.

Motorcycle Insurance Full Coverage: FAQ

Is full coverage motorcycle insurance required by law?

Only liability coverage is legally required in most states. Lenders require full coverage with collision and comprehensive until the loan is paid off. Once you own the bike outright, you can drop collision and comprehensive, though you lose financial protection for the bike's value.

What's the difference between full coverage and liability-only motorcycle insurance?

Liability-only motorcycle insurance covers damage you cause to others but not your own bike. Full coverage adds collision for crash repairs and comprehensive for theft, vandalism and weather damage. Full coverage costs two to three times more but protects the bike's value. Liability-only covers your legal obligation to others only.

Can I add full coverage to my existing motorcycle insurance policy?

Collision and comprehensive coverage can be added to an existing policy at any time by contacting your insurer. Premiums increase immediately, and you'll need to select deductibles for both coverages, typically ranging from $250 to $1,000. Some insurers require a bike inspection before adding comprehensive coverage to verify its condition and prevent fraud.

How do I file a claim with full coverage motorcycle insurance?

For collision claims, contact your insurer within 24 hours of an accident. The insurer will assign an adjuster to assess the damage, verify coverage and authorize repairs up to actual cash value minus your deductible. For comprehensive theft claims, file a police report first, then contact your insurer with the report number. The insurer will pay the actual cash value minus your deductible if the bike is not recovered within 30 days.

Does full coverage pay for a rental motorcycle while mine is being repaired?

No. Full coverage motorcycle insurance doesn’t include rental reimbursement unless you add it as an extra. Rental reimbursement covers about $20 to $40 per day for a temporary bike while yours is in the shop after a collision or comprehensive claim.

If you don’t add this option, you’ll need to pay rental costs yourself or go without a bike during repairs, which usually take two to four weeks.

What deductible should I choose for full coverage motorcycle insurance?

Pick collision and comprehensive deductibles that you can pay from your savings right away. Higher deductibles of $500 to $1,000 lower your full coverage premium by about 20–40%, but you’ll spend more out of pocket when you file a claim.

Lower deductibles of $250 to $500 raise your premium but reduce your cost after a claim. Many riders choose a $500 deductible because it balances monthly cost and out-of-pocket expenses.

Can I get full coverage motorcycle insurance on an older motorcycle?

Most insurers still offer collision and comprehensive coverage for bikes that are 15 to 20 years old, though coverage may be limited if your bike is worth under $2,000 to $3,000.

Since older bikes lose value each year, the payout from a claim also decreases. At some point, full coverage stops being financially practical. Compare the cost of full coverage to your bike’s current market value before adding it to an older motorcycle.

Does full coverage motorcycle insurance protect custom modifications?

Standard collision and comprehensive coverage doesn’t include custom modifications. To protect upgrades like custom exhausts, seats, paint jobs, saddlebags and other parts, you’ll need custom parts and equipment coverage.

This add-on usually covers $3,000 to $10,000 in upgrades. Without it, your insurer reimburses only your bike’s stock value, not the extra $5,000 to $15,000 you invested in customizations.

What is considered full coverage motorcycle insurance?

Full coverage motorcycle insurance includes liability coverage (required in most states), collision coverage (for crash repairs to your bike), and comprehensive coverage (for theft, vandalism, and weather damage).

Together, these three coverages protect both your responsibility to others and your bike’s value, which is why the package is called “full coverage.”

How much is full coverage motorcycle insurance per month?

Full coverage motorcycle insurance costs $30 per month on average nationally, ranging from $10 to $103 monthly depending on your bike's value, age, location, riding history, and coverage limits. The average cost of full coverage motorcycle insurance varies significantly by state, from $17 monthly in Alaska to $156 monthly in Arizona.

How We Analyzed Comprehensive and Collision Motorcycle Insurance

MoneyGeek's complete coverage motorcycle insurance analysis uses comprehensive rate data we gathered from major insurers nationwide. We collected quotes for multiple motorcycle types, rider ages, coverage levels, and locations to determine typical full coverage costs compared to minimum coverage. Our research team contacted insurers directly to verify coverage details, exclusions, and endorsements included in full coverage motorcycle insurance policies.

All cost data in this article, including average full coverage motorcycle insurance costs by age, company, and state, comes from MoneyGeek's proprietary rate analysis conducted in 2025. To provide comprehensive guidance, we evaluated state insurance requirements, insurer financial strength ratings from AM Best, and customer complaint data from state insurance departments.

About Mark Fitzpatrick

Mark Fitzpatrick, a Licensed Property and Casualty (P&C) Insurance Producer in Connecticut, is MoneyGeek's resident insurance expert. He has spent nearly a decade analyzing the market, first at LendingTree and now at MoneyGeek, where he produces original research on hundreds of carriers and millions of rates across auto, home, renters, health and life insurance.

He covers economics and insurance at MoneyGeek, and his work has been featured in The Washington Post, The New York Times and NPR, among other outlets.

Like all MoneyGeek analysts, he draws on independent cost and consumer experience data. No insurance company partnership influences his recommendations.

Mark holds a B.A. from Boston College and an M.A. in Economics and International Relations from Johns Hopkins University. He started his career in financial risk management at State Street and is also a five-time “Jeopardy!” champion.