Term life insurance has a fixed term and a lower price, but no cash value component. Whole life insurance covers the policyholder's entire life at a higher premium but comes with a cash value component that accumulates over time.

Term Life vs. Whole Life Insurance (Cost, Pros and Cons)

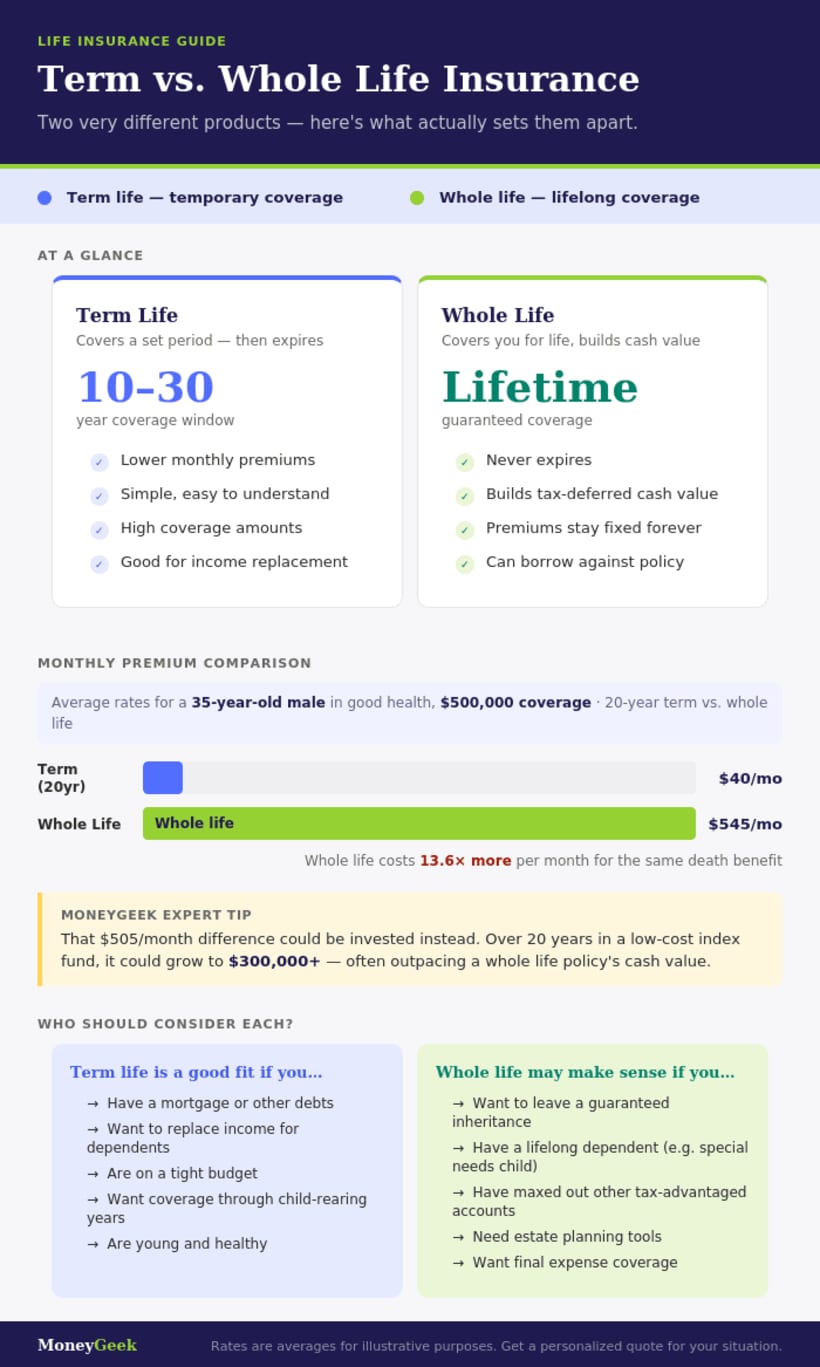

Term life insurance costs less than whole life insurance because it covers you for a set number of years and has no cash value. A 35-year-old man buying $500,000 in coverage pays about $40 a month for a 20-year term vs. $545 a month for whole life, per MoneyGeek's rate analysis.

Select age group

Updated: July 20, 2026

Advertising & Editorial Disclosure

Key Takeaways

Term life insurance is temporary coverage with lower premiums and a death benefit only. It doesn't build cash value.

Whole life insurance provides lifelong coverage, accumulating cash value alongside a death benefit.

Term life offers better value for most buyers. Whole life costs more but makes sense for permanent needs like estate planning or a lifelong dependent.

Differences Between Term and Whole Life Insurance

Coverage duration | Fixed period (10–30 years) | Lifetime |

Premiums | Lower | Higher |

Cash value | None | Builds over time |

Premium structure | Fixed during term; increases at renewal | Fixed for life |

Investment component | None | Cash value grows tax-deferred |

Policy loans | Not available | Can borrow against cash value |

Death benefit taxation | Paid out tax-free | Paid out tax-free |

Dividend eligibility | Not available | Available through mutual insurers (not guaranteed) |

Etate planning utility | Limited; no payout if term ends before death | Strong; can fund trusts, and the death benefit skips probate |

Best for | Young families, temporary needs, budget-conscious buyers | Estate planning, long-term wealth building, guaranteed coverage |

Types of Term Life Insurance

- Level term life insurance: Fixed death benefit and premium for a set term of 10, 20 or 30 years. A practical fit for buyers who want predictable coverage at a consistent cost.

- Decreasing term life insurance: The death benefit decreases over the term, aligned with a mortgage or loan balance. Premiums stay level. A practical fit for homeowners who want coverage tied to a mortgage payoff schedule.

- Annual renewable term life insurance: Renews each year with premiums that increase as the insured ages. A practical fit for short-term or temporary coverage needs.

- Convertible term life insurance: Can be converted from term to whole life without a new medical exam.

Types of Whole Life Insurance

- Traditional whole life insurance: Fixed premiums, a set death benefit and steady cash value growth. A practical fit for buyers who want simplicity and guaranteed growth.

- Variable whole life insurance: Cash value is invested in sub-accounts similar to mutual funds. Suitable for buyers who are comfortable with investment risk in exchange for higher growth potential.

- Single-premium whole life insurance: The full premium is paid upfront in exchange for a guaranteed death benefit and immediate cash value accumulation.

- Limited payment whole life insurance: Premiums are paid over a fixed period with lifetime coverage remaining in place.

Cost of Term Life vs. Whole Life

Whole life costs more than term life insurance, and the difference increases as you get older. The table below compares average monthly rates based on quotes we collected for $500,000 term and whole life policies. Term pricing reflects policies with a 20-year term.

25 | $28 (F) / $34 (M) | $310 (F) / $364 (M) | $282 more (F) / $330 more (M) |

30 | $29 (F) / $36 (M) | $399 (F) / $444 (M) | $370 more (F) / $408 more (M) |

35 | $34 (F) / $40 (M) | $490 (F) / $545 (M) | $456 more (F) / $505 more (M) |

40 | $46 (F) / $55 (M) | $605 (F) / $667 (M) | $559 more (F) / $612 more (M) |

45 | $66 (F) / $84 (M) | $767 (F) / $856 (M) | $701 more (F) / $772 more (M) |

50 | $95 (F) / $128 (M) | $1,025 (F) / $1,146 (M) | $930 more (F) / $1,018 more (M) |

55 | $143 (F) / $201 (M) | $1,322 (F) / $1,505 (M) | $1,179 more (F) / $1,304 more (M) |

60 | $250 (F) / $254 (M) | $1,738 (F) / $2,052 (M) | $1,488 more (F) / $1,798 more (M) |

*Rates shown are averages for nonsmokers of average height, weight and health.

Term vs. Whole Life Insurance: Pros and Cons

Benefits of Term Life vs. Whole Life

Benefits of term life insurance:

- Lower cost: Term life costs less than whole life because coverage is temporary and no cash value accumulates.

- Fixed death benefit: Pays a set amount to beneficiaries if the policyholder dies during the term.

- Level premiums: Premiums stay the same for the life of the policy.

- Rider eligibility: Term policies qualify for riders, though available options vary by insurer.

Benefits of whole life insurance:

- Lifetime coverage: Whole life covers the policyholder for life as long as premiums are paid.

- Cash value: Whole life policies build cash value the policyholder can borrow against or withdraw at any time. Growth is tax-deferred.

- Guaranteed death benefit: Pays regardless of when the policyholder dies.

- Fixed premiums: Premiums stay the same for the life of the policy.

- Dividend eligibility: Policyholders at mutual insurers may receive dividends when the company turns a profit. Dividends aren't guaranteed.

- Estate planning utility: Whole life doesn't expire, so it can anchor an estate plan in ways term life can't.

Drawbacks of Term Life vs. Whole Life

Drawbacks of term life insurance:

- Limited duration: Coverage ends when the term does. Renewing or buying a new policy costs more as you age.

- No cash value: Pays only a death benefit with no savings or investment component.

- Premiums increase at renewal: Applies to annual renewable term policies.

- Fewer options: Fewer riders and coverage adjustment options than whole life.

Drawbacks of whole life insurance:

- Higher cost: Whole life premiums are 5 to 15 times higher than comparable term coverage. A 35-year-old buying $500,000 in whole life pays roughly $505 more a month than for a comparable term policy. This means over $121,000 more in premiums over 20 years, not counting what that money could have earned if invested.

- Lower investment returns: Cash value growth tends to be slower than market returns on comparable investments like index funds.

- Rigid payment schedule: A missed premium can reduce the death benefit or lapse the policy.

- Cash value stays with the insurer at death: Accumulated cash value not withdrawn or borrowed before death goes to the insurer. Beneficiaries receive only the death benefit.

Who Should Get Term or Whole Life Insurance?

For most people, term life is the smarter financial move, but there are some cases where whole life makes sense.

Choose term life if you:

- Want the most affordable coverage

- Only need coverage for a specific period, such as until your mortgage is paid off or your children are financially independent

- Is the primary income earner for a young family on a tight budget

- Don't need a savings or investment component built into your policy

- Want to invest the premium difference elsewhere on your own terms

Choose whole life if you:

- Need coverage that lasts your entire life, regardless of when you die

- Have a lifelong dependent, such as a child with a disability, who will require financial support after you're gone

- Want to use life insurance as part of an estate plan to fund a trust, leave an inheritance, or pass assets to the next generation

- Have maxed out tax-advantaged retirement accounts and want an additional tax-deferred savings vehicle

- Can comfortably afford premiums 5 to 15 times higher than a comparable term policy for the rest of your life

WHOLE VS. TERM LIFE INSURANCE FOR SENIORS

For seniors, the decision depends on financial obligations and long-term goals. Term life is a better fit when there are specific debts or time-limited obligations remaining. Whole life is a better fit for estate planning or legacy purposes.

Buy Term and Invest the Rest

"Buy term and invest the rest" means buying a lower-cost term policy for death benefit coverage and putting the premium savings into a 401(k), IRA or index fund. Term premiums are substantially lower than whole life, and market-linked investments have historically outpaced the fixed returns on whole life cash value. For disciplined investors who consistently invest the difference, this approach can build more wealth than the cash value component of a whole life policy over time.

The strategy has limitations. It requires consistent follow-through over many years, and the savings often get spent rather than invested. It also doesn't account for the risk of becoming uninsurable when term coverage expires or the effect of a market downturn near the end of the policy term. Whole life's guaranteed premiums, guaranteed cash value growth and permanent coverage are worth the higher cost for buyers who value certainty over potential upside.

Switching Life Insurance Policies

Life insurance needs change, and switching policies is more common than most people think. Here's how each direction works.

- Switching from term to whole life: A convertible term policy allows the switch without a new medical exam. This is a common path for buyers whose needs have become permanent.

- Switching from whole to term life: The switch lowers premiums but forfeits accumulated cash value. It makes sense when obligations have decreased — children grown, mortgage nearly paid off, no remaining need for permanent coverage. Any surrender value above the premiums paid in may be taxable. Consult a tax professional before making the change.

- Laddering policies: Some buyers pair a permanent whole life base with one or more term layers on top. The whole life policy covers lifelong needs. A 20-year term layer covers a larger temporary need like a mortgage or income replacement during peak earning years. As each term layer expires, total coverage decreases in line with shrinking obligations. The whole life base stays in place.

Term vs. Whole Life Insurance : FAQ

Term life insurance covers a fixed period (10 to 30 years) and pays a death benefit to beneficiaries if the policyholder dies during that term. It has no cash value component, which keeps premiums lower than whole life.

Whole life insurance provides permanent coverage with a guaranteed death benefit and a cash value component that grows tax-deferred. Premiums are fixed but higher than term life.

For most people with temporary coverage needs, term life is the better value: lower premiums, same death benefit protection. Whole life is worth the higher cost if you need permanent coverage or want a tax-advantaged savings component.

Yes. You can access whole life cash value three ways: surrender the policy for its accumulated cash value minus any surrender charges, take a policy loan against the cash value while keeping the policy in force or make a partial withdrawal without ending the policy.

Your beneficiaries receive the policy's death benefit, not the death benefit plus the cash value. If you die without withdrawing or borrowing the accumulated cash value, the insurer keeps it. This is one of the most commonly misunderstood features of whole life insurance.

For most people with straightforward coverage needs, no. Term life delivers the same death benefit protection at a fraction of the cost. Whole life is worth considering if you need permanent coverage, have a lifelong dependent, want a guaranteed tax-deferred savings vehicle after maxing out retirement accounts or are using life insurance as a cornerstone of an estate plan.

MoneyGeek collected quotes for $500,000 in coverage for term and whole life insurance. Rates are for nonsmokers in average health. Term figures are based on 20-year level term policies. Whole life figures are for traditional whole life policies with level premiums. Individual rates vary by health class, state and insurer, so a personalized quote will differ from the averages shown here.

Related Pages

About Mark Fitzpatrick

Mark Fitzpatrick, a licensed Property and Casualty (P&C) Insurance Producer in Connecticut, is MoneyGeek's resident expert in insurance and economics. He has spent nearly a decade covering the market, first at LendingTree and now at MoneyGeek, where he analyzes hundreds of carriers and millions of rates across auto, home, renters, health and life insurance.

His work has appeared in The Washington Post, The New York Times and NPR. He draws on independent cost and consumer experience data, and no insurance company partnerships influence his recommendations.

Mark studied at Boston College before earning a master's in economics and international relations from Johns Hopkins University. Before MoneyGeek, he worked in financial risk management at State Street. He's also a five-time “Jeopardy!” champion.