Chubb is Pensacola's best home insurance company after we evaluated insurers considering affordability, coverage options and customer experience ratings. Our analysis identified providers offering the best value and service for local homeowners.

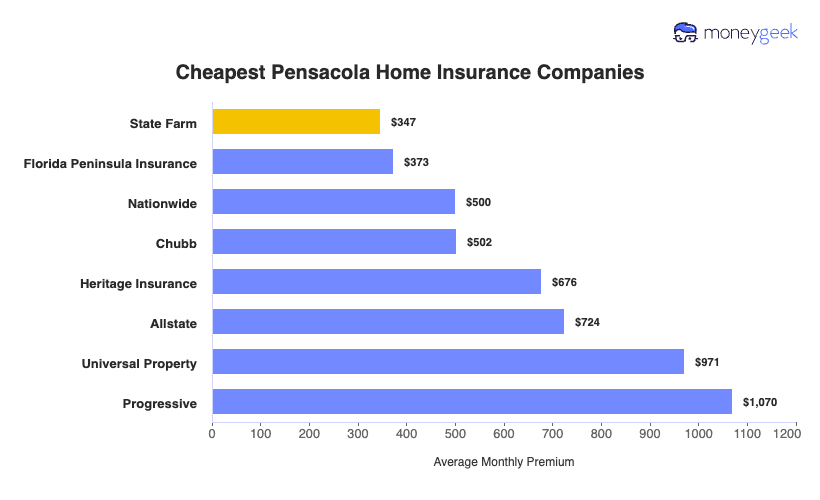

- Chubb

- State Farm

- Nationwide

- Allstate

- Florida Peninsula