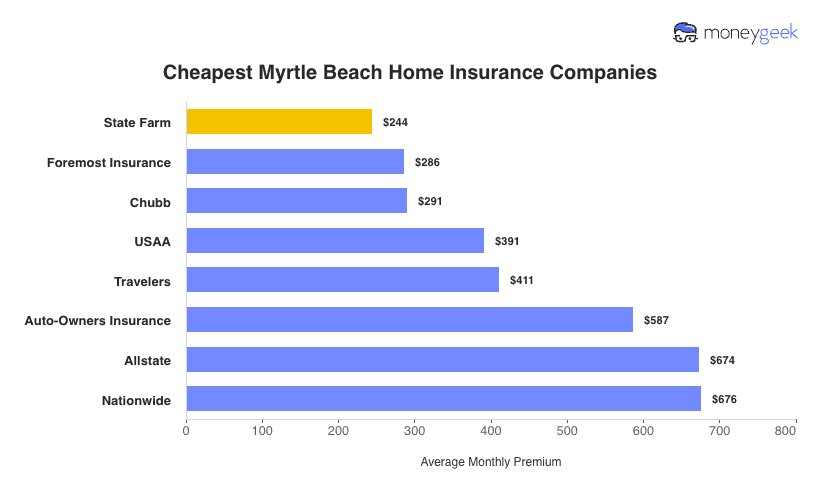

Chubb leads as Myrtle Beach's best home insurance company based on affordability, coverage options and customer experience. USAA, State Farm, Auto-Owners and Foremost round out the top five for local homeowners.

- Chubb

- USAA

- State Farm

- Auto-Owners

- Foremost