We evaluated insurers considering customer experience ratings, affordability and coverage options to find McKinney's best providers. State Farm ranks as the best home insurance company for local homeowners.

- State Farm

- USAA

- Chubb

- Farmers

- Mercury

Updated: March 1, 2026

Advertising & Editorial Disclosure

State Farm ranks as McKinney's best home insurance provider, while other top-rated home insurance companies include USAA, Chubb, Farmers and Mercury Insurance for local homeowners.

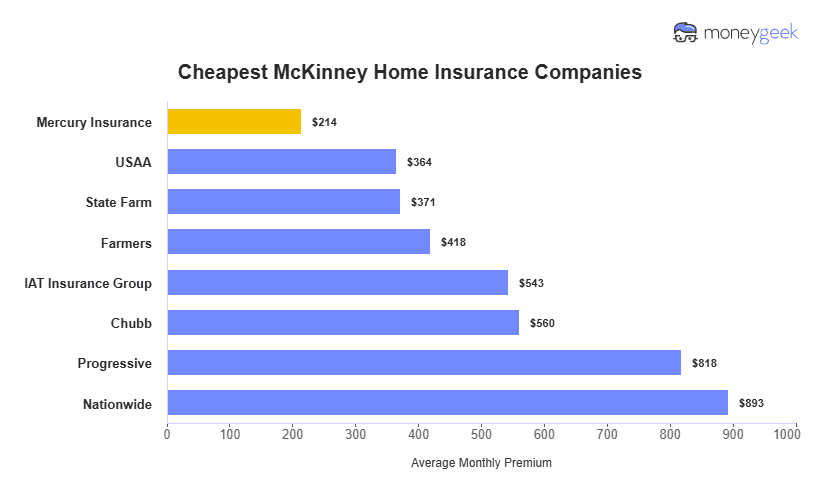

Mercury Insurance offers McKinney's most affordable home insurance according to our research, with rates averaging $2,574 per year.

Finding affordable McKinney home insurance requires determining your coverage needs, researching companies and costs, then comparing quotes from multiple insurers.

We evaluated insurers considering customer experience ratings, affordability and coverage options to find McKinney's best providers. State Farm ranks as the best home insurance company for local homeowners.

| State Farm | 4.54 | $371 | -29% |

| USAA | 4.86 | $364 | -30% |

| Chubb | 4.5 | $560 | 7% |

| Farmers | 4.39 | $418 | -20% |

| Mercury Insurance | 4.25 | $214 | -59% |

*Rates are for a 2,500-square-foot home built in 2000, with $250,000 of dwelling coverage and a $1,000 deductible.

**Although USAA earned the highest score from our team, we ranked it No. 2 because coverage isn't available to all McKinney residents.

Average Annual Premium

J.D. Power Customer Satisfaction Score

Number of Discounts

McKinney homeowners pay $523 monthly for home insurance with $250,000 in dwelling coverage, which is 7% lower than the Texas average cost of $560. Despite the city's growing population and increased flood risks from nearby waterways, residents pay more affordable premiums than in most Texas cities. Mercury Insurance offers the most affordable coverage at $214 monthly, saving McKinney homeowners $309 compared to the city average.

Mercury consistently offers the most affordable rates across most McKinney homeowner profiles, though your actual rate depends on coverage needs, credit score and claims history.

This guide shows you how to get cheap homeowners insurance without sacrificing protection.

Building materials in McKinney influence your dwelling coverage needs. Too little coverage leaves you exposed after serious damage, but too much coverage means paying for protection you don't need.

Basic coverage includes wind and hail protection, but check that limits adequately cover tornado and hail damage common in McKinney. Add flood insurance through your insurer or the National Flood Insurance Program and verify wind coverage limits are high enough to cover rebuilding costs.

Check J.D. Power scores for claims handling, review the NAIC complaint index for problems and look at customer reviews on Trustpilot.

Request quotes from at least three insurers with the same coverage to find your best rate. Make sure you're comparing identical coverage limits and deductibles for accurate pricing.

Higher deductibles lower your monthly premiums but increase out-of-pocket costs when you file a claim. Choose a deductible you can afford to pay if disaster strikes.

Home values, construction costs and personal belongings change over time, affecting your insurance needs. Review your policy each year before renewal.

We answer common questions about McKinney home insurance:

Major life changes like home improvements, expensive purchases or rising construction costs should trigger a coverage review. McKinney's building costs have increased , so your dwelling coverage from a few years back might not fully replace your home today.

Your standard homeowners policy covers wind damage from hurricanes, while flood damage needs separate flood insurance. You'll pay different deductibles for each: wind damage carries a 1% to 5% deductible based on your dwelling coverage amount.

Actual cash value factors in depreciation when paying claims, meaning you'll receive less money for older roofs, appliances and belongings. Replacement cost coverage pays today's full price to rebuild or replace damaged items without deducting for age or wear.

Older roofs drive up insurance costs — insurers charge higher premiums once your roof hits 15 years, and many won't cover homes with roofs over 20 years old. A professional roof inspection that shows good condition can help you avoid coverage denials or steep rate increases.

We analyzed home insurance premiums from 10 companies in McKinney using data from Quadrant Information Services. Customer satisfaction scores came from J.D. Power surveys to identify insurers with low rates and reliable claims service.

Base Profile Details

Our analysis used a standard McKinney homeowner profile:

This profile represents a typical McKinney homeowner and allows for accurate rate comparisons across insurers.

Why This Matters for Your Decision

Comparing identical coverage levels across companies shows which insurers offer the best value. A company advertising low rates might only be cheap for excellent credit scores or newer homes. Our multi-scenario approach shows you what you'll actually pay based on your situation, not just advertised rates that don't apply to you.

About Mark Fitzpatrick

Mark Fitzpatrick, a Licensed Property and Casualty Insurance Producer, is MoneyGeek's resident Personal Finance Expert. He has analyzed the insurance market for over five years, conducting original research for insurance shoppers. His insights have been featured in CNBC, NBC News and Mashable.

Fitzpatrick holds a master’s degree in economics and international relations from Johns Hopkins University and a bachelor’s degree from Boston College. He's also a five-time Jeopardy champion!

He writes about economics and insurance, breaking down complex topics so people know what they're buying.