MoneyGeek's investment calculator estimates your investment balance over time. Enter your initial deposit, contribution details, expected return rate and compound frequency. The calculator shows cumulative totals for principal and interest so you can see exactly how each factor affects long-term growth. Adjust values to test different scenarios and find the strategy that works for your goals.

Investment Calculator

Use MoneyGeek's free investment calculator to estimate your investment balance. Enter your initial deposit and contribution amounts, contribution frequency, and other details to see how your money could grow over time.

Total Balance

$0

YEAR

Total principal

Investment Growth and Return Calculator

Updated: May 25, 2026

Advertising & Editorial Disclosure

How to Use MoneyGeek’s Investment Calculator

Enter your investment details to see how your money could grow over time.

- 1Set Your Initial Deposit and Contributions

Your initial deposit forms the foundation of your investment. Enter the amount you're starting with, and all future gains build from this base. Add your contribution amount and choose monthly or annual frequency. Regular contributions grow your balance and expand total returns over time. Monthly contributions compound more often and build your balance faster. Annual contributions compound less frequently but still add long-term value.

The calculator treats contributions as if made at the end of each period. End-of-period contributions reflect standard deposit timing, where money enters accounts after the period completes. Beginning-of-period contributions would compound slightly faster, but most financial calculators use end-of-period as the standard assumption.

- 2Define Your Investment Timeline

Enter your investment period in years. Longer time frames let compound interest work through more cycles. A 25-year-old investing for 40 years builds a larger balance than someone investing for 20 years, even with the same contributions.

- 3Input Your Expected Rate of Return

Use average return rates that match your investment type and risk tolerance. For conservative projections, use 4% to 5%. Moderate growth portfolios average 6% to 7% a year. Stocks average 9% to 10% (S&P 500 Index average), while diversified bond portfolios average closer to 5%. Choose a rate that reflects your actual asset mix and comfort with market volatility.

- 4Select Your Compound Frequency

Choose how often interest compounds on your investment. Monthly compounding applies interest more often and builds your balance faster over time. Daily compounding maximizes growth for larger or longer-term investments. Each application compounds on prior gains as well as the original balance, so more frequent compounding adds up over time.

How to Read the Results

The calculator displays three figures: Total Balance (your investment's overall value), Total Principal (amount you contributed) and Total Interest (what you earned from compounding). The graph tracks growth over time and shows how contributions and interest build on each other. An upward trend means growth is on track. If the line flattens, consider adjusting your contributions, timeline or expected return.

SAMPLE CALCULATION

Starting with $5,000 and adding $200 monthly at a 6% annual return compounded monthly over 10 years yields around $41,873. Your contributions total $29,000, while compounding interest adds $12,873. Interest compounds on both your initial deposit and each monthly contribution. Growth builds on itself with each cycle. Even small changes to your timeline or monthly amount can shift your ending balance by thousands.

Why Use an Investment Calculator?

MoneyGeek's investment calculator estimates potential returns, explores different contribution strategies and helps you plan for long-term financial growth.

Estimate and Visualize Investment Returns

Estimate and Visualize Investment ReturnsEstimate how much your investment will grow over time based on your starting amount and regular contributions.

Plan for Retirement

Plan for RetirementIf you're thinking about retirement, this tool helps you figure out how much you need to save to reach your goals. Test different scenarios, like adjusting your monthly contributions or expected return, to match your retirement plans. As your investment portfolio grows, consider life insurance to protect the wealth you're building. Adequate coverage lets your family maintain financial stability and continue funding long-term goals if something happens to you.

Optimize Contribution Strategies

Optimize Contribution StrategiesExperiment with contribution frequency or amount to see how small changes boost growth. Monthly contributions of $250 versus $200 can add thousands to your final balance. Consistent contributions accelerate returns and get you to your financial goals faster.

Account for Taxes and Inflation

Account for Taxes and InflationInvestment calculators show nominal returns, but taxes and inflation reduce actual purchasing power. A 7% return with a 25% combined tax rate and 3% inflation yields roughly 2.25% in real after-tax growth. Use the real return figure, not the nominal rate, to set your contribution targets.

Compare Different Investment Scenarios

Compare Different Investment ScenariosRun a conservative 5% projection alongside an aggressive 9% one to see how much the difference compounds over 20 years. A strategy that matches your risk tolerance is one you'll stick with.

Types of Investments

The calculator projects growth for stocks, bonds, real estate and commodities. Each type has unique potential returns and risks.

Type | Description | How to Use the Calculator |

|---|---|---|

Stocks | Stocks represent company ownership with returns from price appreciation and dividends, averaging 9% to 10% a year (S&P 500 Index). | Start with your initial amount and monthly contribution. Use a 9% to 10% return rate as a benchmark for long-term stock portfolios. |

Mutual Funds | Mutual funds pool investor money to buy diversified assets across many companies, lowering individual risk. Returns vary by fund focus (equity funds ~9% to 10%, bond funds ~5%). | Add your initial investment and monthly contributions. Use a rate matching your fund type (equity or bond) to project growth. |

Bonds | Bonds provide predictable interest income through corporate or government debt, with diversified portfolios averaging 5% a year. | Enter your deposit and contribution amount. Use a 5% rate to model steady bond interest compounding over time. |

Real Estate | Real estate investment provides returns through property appreciation and rental income, with private commercial real estate yielding 8% to 12% a year over the long term. | Input your property investment and planned contributions. Use an 8% to 12% growth rate to project value appreciation and rental income. |

Commodities | Commodities like gold, oil and agricultural goods serve as inflation hedges, with gold averaging 7% to 8% annual returns since the 1970s, though prices can swing widely. | Set your initial investment and expected return range. The calculator models value changes based on price fluctuations over time. |

Different investments compound at different frequencies. Stocks and mutual funds: Use daily compounding for modeling purposes (actual returns are driven by market prices and reinvested dividends). Bonds and savings accounts: Match your account's stated compound frequency. Most accounts compound monthly. Real estate and commodities: Annual compounding reflects standard valuation cycles for these asset classes.

Managing Investment Risk

Investment returns aren't guaranteed, and market volatility can drag down short-term performance. Diversification spreads money across stocks, bonds, real estate and commodities to reduce that risk. One underperforming sector won't sink the whole portfolio when others are holding up.

Your asset allocation should match your timeline and risk tolerance. Younger investors often hold 80% to 90% stocks for growth, which means accepting more short-term swings for stronger long-term gains. Those nearing retirement shift toward 50% to 60% bonds for stability. That balance protects accumulated wealth from market swings.

Rebalancing annually maintains your target allocation as different investments grow at different rates. It prevents overexposure to any single asset class and curbs emotional decisions during market downturns.

Dollar-cost averaging means investing a fixed amount on a regular schedule, regardless of market conditions. It reduces timing risk and builds positions whether prices are up or down. Over time, regular contributions through market cycles outperform most attempts to time the market.

Investment Growth vs. Investment Return

Investment growth and return measure different aspects of performance.

Investment growth tracks your total balance over time: initial deposit, regular contributions, compounded interest and reinvested earnings like dividends.

Investment return measures the percentage gained relative to your initial deposit. It tracks income from your starting capital, including dividends, and excludes additional contributions.

SAMPLE SCENARIO: GROWTH VS. RETURN

Start with $10,000 and add $500 monthly at a 5% annual return compounded monthly over 10 years.

Investment growth: After 10 years, your balance reaches around $94,111. This includes your initial $10,000 deposit, all monthly contributions ($60,000 total) and $24,111 in compounded interest.

Investment return: Your initial $10,000 deposit earns around $500 in the first year, a 5% return. This measures only what your starting capital generates, excluding monthly contributions. Growth tracks everything in your portfolio. Return is specific to your original deposit.

Investment Calculator FAQ

Find answers about choosing a return rate, calculating ROI and planning your investment period.

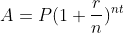

The basic investment formula is:

This equation calculates your investment's future value. A is your ending balance, P is your initial investment, r is the annual interest rate (as a decimal), n is how many times interest compounds per year, and t is how many years you invest.

Investment calculators provide estimates based on your inputs, but actual returns vary with market conditions, fees and taxes.

To calculate return on investment (ROI), divide net profit by initial investment and multiply by 100 to get a percentage. Earning $1,000 on a $10,000 investment, for example, yields a 10% ROI.

Review your investments at least once a year. A new job, home purchase or change in your retirement timeline also calls for a review.

Taxes reduce your effective return. Capital gains taxes apply when you sell investments for profit. Long-term rates (held over one year) range from 0% to 20% based on income, while short-term gains are taxed as ordinary income, up to 37%. Dividend income and interest are also taxable. Tax-advantaged accounts like 401(k)s and IRAs defer or eliminate these taxes. Those savings compound over time.

Nominal returns show percentage gains without adjusting for inflation. Real returns account for inflation's impact on purchasing power. A 7% nominal return with 3% inflation yields a 4% real return. That figure reflects your actual wealth increase and buying power over time.

Monthly contributions compound more frequently and generate slightly higher returns over time. A $6,000 annual contribution ($500 monthly) compounded monthly outperforms a single $6,000 yearly deposit. They also smooth out market volatility through dollar-cost averaging and align with most paycheck schedules.

Find Additional MoneyGeek Calculators

About Nathan Paulus

Nathan Paulus is Head of Content and SEO at MoneyGeek, where he leads content strategy and produces original data research across insurance, consumer costs, transportation safety, housing, public policy and personal finance. He also reviews published studies for methodology, source quality and factual accuracy before they reach readers.

Research and Analysis

In nearly six years at MoneyGeek, Nathan has published more than 100 original studies and explanatory guides. His insurance research includes 50-state comparisons of health care outcomes, costs and access, plus an analysis of how uninsured rates track with state Medicaid expansion decisions and electoral patterns. He has analyzed full coverage auto rates across major insurers in all 50 states and how premium trends track with industry underwriting losses, using combined ratio data from Fitch Ratings, AM Best and Bureau of Labor Statistics CPI figures. Beyond insurance, his work spans vehicle pricing trends across the U.S. new car market, summer traffic fatality rates by state, homeowner underinsurance ratios using mortgage and policy data, and housing affordability across all 50 states.

His research has been cited by Bloomberg, the Los Angeles Times, Forbes, Fast Company, the San Francisco Chronicle, USA Today and NBC Los Angeles. Harvard, MIT, Stanford and Yale have also referenced his work.

Career

Nathan traces his interest in personal finance back to his grandmother, who ran her household on a simple rule: spend less than you make, and save the difference before anything else. That rule shows up in his work today. His writing skips jargon and complex strategy in favor of the basics that help someone living paycheck to paycheck.

He joined MoneyGeek in July 2020 as Director of Content Marketing, leading the content team and directing data journalism production across insurance and personal finance verticals. A promotion to Head of Marketing and Communications followed in December 2023, adding digital PR and communications strategy to his role. He has held his current title, Head of Content and SEO, since January 2025.

Before MoneyGeek, Nathan served as Director of Content Marketing and SEO at Ventrix Advertising, where he helped build two content sites from scratch, contributed to link-building programs that secured more than 1,500 unique referring domains within a year, and co-managed a marketing team of more than 20 people. Before that, two and a half years at ABUV Media took him from Marketing Research Analyst to Senior Marketing Tactics Analyst, where he built his grounding in audience research, content strategy and SEO.