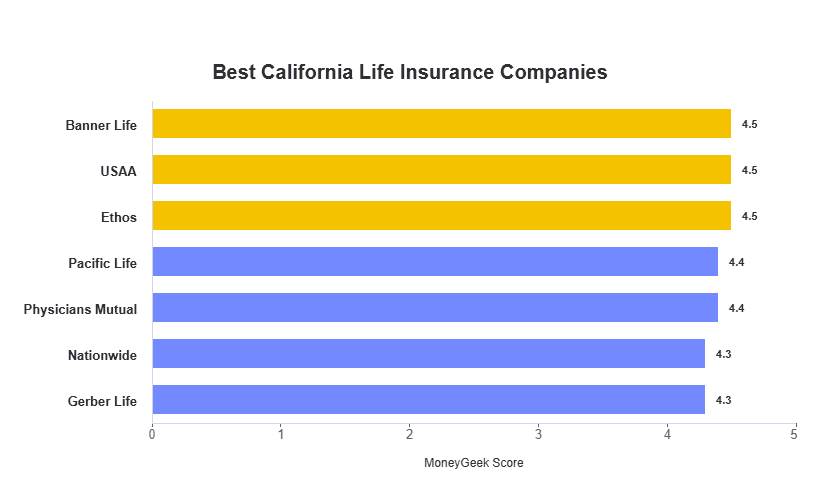

We reviewed over 30 life insurance companies, thousands of quotes, policy options and customer reviews to find the best life insurance providers in California. The seven providers below represent the best combination of monthly rates, coverage flexibility, financial strength and customer experience we found in the state.

California's life insurance market is one of the most competitive in the country, with heavy variation in rates and underwriting standards across carriers. Banner Life is our top pick for term coverage, with rates 21% to 22% below the state average for 40-year-olds. USAA leads for permanent coverage with an A++ AM Best rating and flexible payment options. Ethos is the fastest path to coverage with same-day approval and no medical exam. Pacific Life is best for high coverage needs up to $10 million. For families, Gerber Life covers parents and children under one plan. Nationwide has the lowest rates for buyers in their 20s, and Physicians Mutual is our top choice for guaranteed issue coverage. Every provider on this list holds an A+ or better AM Best rating.